Re: File No. S7-07-15 — Proposed Rule to Implement Section 953(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010

Dear Mr. Fields:

Meridian Compensation Partners, LLC (“Meridian”) is pleased to provide comments to the Securities and Exchange Commission (“Commission”) on the Commission’s proposed rule to implement the provisions of Section 953(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (“Dodd-Frank Act”).

Meridian is one of the largest independent executive compensation consulting firms in North America. We provide trusted counsel to Boards and Management at hundreds of large public and private companies, consulting on executive compensation design issues, corporate governance matters and related disclosures. Our consultants have decades of experience in developing pay solutions that are responsive to shareholders, reflect good governance practices and align with company performance.

Section 953(a) of the Dodd-Frank Act directs the Commission to amend Item 402 of Regulation S-K (“Item 402”) to require registrants (subject to certain exceptions) to disclose in a clear manner the relationship between executive compensation actually paid and the financial performance of the registrant (referred to herein as the “Pay versus Performance Disclosure”).

On April 29, 2015, the Commission issued proposed amendments to Item 402 to add the Pay versus Performance Disclosure requirement (Pay Versus Performance Disclosure, Release No. 34-74835 (May 7, 2015) [80 FR 26330] (referred to herein as the “Release”)). Set forth below are our comments on the proposed amendments (“Proposed Rule”).

Summary of Recommended Changes to the Proposed Rule

The following is a summary of Meridian’s recommended changes to the Proposed Rule, which is followed by a detailed rationale for each of these recommendations.

- Eliminate the required tabular disclosure in favor of a graphical disclosure depicting registrant total shareholder return (TSR) and compensation actually paid over the covered period.

- Limit the scope of the required disclosure to a registrant’s principal executive officer (PEO) and Principal Financial Officer (PFO).

- Base the amount “actually paid” under a stock option grant on the option’s in-the-money value on the date of vesting.

- Eliminate (or modify) the disclosure of peer group TSR.

The Proposed Rule would add to the ever-expanding size of registrant proxies. We would anticipate that the required disclosures (i.e., the required tabular and explanatory disclosures) and likely volitional disclosures could increase proxy filings of large public companies by several pages. These disclosures would be in addition to the proxy disclosures that will be required under Section 953(b) (CEO Pay Ratio), Section 954 (Mandatory Clawback Policy) and Section 955 (Hedging Policy) of the Dodd-Frank Act. In fashioning a Final Rule, we strongly urge the Commission to remain mindful of the cumulative impact these additional disclosures will have on the length and readability of a registrant’s proxy statement.

Recommended Changes to the Proposed Rule

We are recommending that the Commission revise the Proposed Rule in the following manner for the reasons indicated:

Eliminate the required tabular disclosure in favor of a graphical disclosure.

For the reasons discussed below, we recommend that the Commission eliminate the proposed tabular disclosure and, in lieu thereof, require a graphical disclosure showing registrant TSR and compensation actually paid.

The centerpiece of the Proposed Rule would be a tabular disclosure that presumably is intended to facilitate an investor’s understanding of the link between executive pay and a registrant’s performance. However, the format and scope of the proposed disclosure undermines this objective. The proposed table would more likely serve to confuse rather than enlighten investors as to the relationship between executive pay and corporate performance.

A tabular format is particularly ill-suited for communicating the relationship between changes in two or more variables (e.g., changes in executive pay and changes in registrant performance). Further undermining the clarity of the proposed table would be the requirement for a registrant to include unnecessary data and information (i.e., PEO SCT total compensation, other named executive officers’ average SCT total compensation and cumulative TSR data on the registrant’s peer group).

The Commission appears to acknowledge these shortcomings by requiring a registrant to decipher the table through a mandated explanatory disclosure and any volitional disclosures thought necessary by a registrant. Under the Proposed Rule, a registrant would be permitted to make the required explanatory disclosure in any format or combinations of formats (e.g., narrative, graphical). In the Release, the Commission provides various examples of potential formats for this disclosure.[1] This disclosure regime would needlessly add to the complexity and length of a registrant’s Pay versus Performance Disclosure, while undermining the comparability of the disclosure across registrants.

Given the drawbacks inherent in the proposed tabular disclosure, we recommend that the Commission revise the Proposed Rule to require disclosure of pay and performance information in a uniform graphical format across registrants. This recommended graphical disclosure would plot a registrant’s cumulative TSR over the applicable covered period and would show compensation actually paid each covered year to a registrant’s PEO and PFO (see discussion below with regard to limiting the Proposed Rule to a registrant’s PEO and PFO) as a bar column. In addition, we recommend that the Commission revise the Proposed Rule to provide that a registrant would be required to include in a footnote to the foregoing graphical disclosure a complete reconciliation between compensation actually paid to a registrant’s PEO and PFO and total compensation of the PEO and PFO reported in the registrant’s Summary Compensation Table. The recommended graphical disclosure and footnote thereto would cover all the data points required to be included in the proposed tabular disclosure, except for data relating to peer group TSR (see discussion below with regard to eliminating, or modifying, the disclosure of peer group TSR).

The recommended disclosure would clearly and concisely show the relationship between executive pay and registrant TSR performance. Further, this recommended disclosure would likely mitigate the need for registrants to make other graphical disclosures, as is currently contemplated under the Proposed Rule and would likely minimize the complexity and length of any accompanying narrative explanatory disclosure and volitional disclosure. Other benefits that would be realized from substituting the recommended graphical disclosure for the proposed tabular disclosure include the following:

-

- Enhanced comparability of disclosures across covered years for a registrant and across registrants.

- Reduced burden in producing the required disclosure.

- Reduced length of overall disclosure.

Limit the scope of the required disclosure to a registrant’s PEO and PFO.

For the reasons discussed below, we recommend that the Commission revise the Proposed Rule so that it solely applies to a registrant’s PEO and PFO.

As noted in the Release, Securities Exchange Act of 1934 Section 14(i) does not specify which executives must be covered by the Pay versus Performance Disclosure.[2] The Commission is proposing that the Pay versus Performance Disclosure requirement apply to each of the registrant’s named executive officers. Specifically, the Proposed Rule would require a registrant to disclose compensation actually paid to its PEO and the average compensation actually paid to its other named executive officers[3] (“Average NEO Compensation”). In the Release, the Commission states that the proposed disclosure of the relationship between Average NEO Compensation and registrant performance would be more meaningful to shareholders than the disclosure of individual or aggregate named executive officer compensation to registrant performance.[4] In addition, the Commission contends that the use of Average NEO Compensation would help make the information about named executive officers, other than the PEO, more comparable from year to year in spite of the potential variability in the composition and number of such named executive officers over the years for which disclosure is required.[5]

Implied by the Commission’s rationale is that the rate and direction of change in compensation actually paid to individual named executive officers (other than to the PEO) of a registrant is broadly similar over a covered disclosure period. If that were not the case, then comparisons between Average NEO compensation and registrant performance would not likely yield meaningful insights into the relationship between those two measures. The Commission has presented no empirical analysis supporting this implicit rationale for requiring the disclosure of Average NEO Compensation.

Common experience shows that rate and direction of change in compensation paid to individual named executive officers of a registrant does not move in lock step and may often materially differ among named executive officers. A broad variety of factors impact changes in executive officer pay. These factors are not likely to be uniform among individual executive officers. For example, pay level, pay mix, performance objectives and individual performance may materially differ among individual named executive officers. These differences may lead to widely disparate changes in pay among individual named executive officers.

Further complicating matters, the composition and number of named executive officers may fluctuate year over year. For example, one or more of the positions represented by the three highest paid named executive officers (other than the PEO and PFO) disclosed in a registrant’s Summary Compensation Table could change dramatically over the five-year period covered under the Proposed Rule. The pay structure and pay levels of a newly included executive officer may differ substantially from the replaced executive officer. Many other factors can impact the comparability of NEO compensation levels, including bonus, severance benefits and retention grants and promotions, among others.

Despite the foregoing issues regarding variability of changes in compensation among named executive officers and composition of the named executive officer group, the Commission asserts that the use of Average NEO Compensation would enhance the comparability of disclosed pay data. We believe that would not be the case and that the Commission’s proposed use of Average NEO Compensation would undermine the comparability of pay data across covered years.

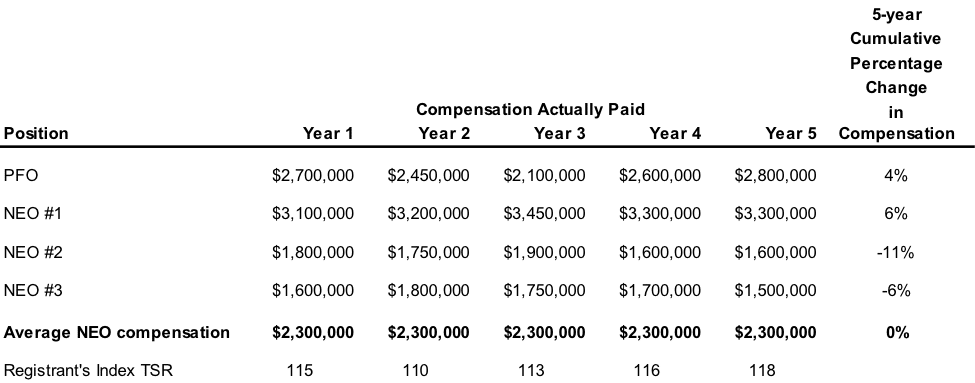

Given the potential for named executive officer pay to change at different rates and in different directions, Average NEO Compensation would not provide investors insight as to the relationship between compensation actually paid to named executive officers, either on an individual or group basis, and registrant performance. The following hypothetical example is illustrative of this point:

The foregoing table shows the determination of Average NEO Compensation based on hypothetical levels of compensation actually paid to each named executive officer (other than the PEO) of a registrant each covered year. The table also shows annual changes in the registrant’s index TSR. To help illustrate the shortcomings of using Average NEO Compensation, the table also shows the 5-year cumulative percentage change in each named executive officer’s compensation.

Based on the foregoing compensation data, the registrant would report the same level of Average NEO Compensation for each covered year pursuant to the Proposed Rule. This disclosure would not illustrate the actual rate of change in compensation paid to each individual named executive officer over the covered five-year period. Although the likelihood of this precise scenario actually occurring may not be high, the example does illustrate that averaging compensation of the named executive officers (other than the PEO) could potentially distort the relationship between named executive officer compensation and registrant performance. As such, we believe that the proposed disclosure of Average NEO Compensation could mislead investors with regard to the actual relationship between named executive officer compensation and registrant performance.

A straightforward solution to the foregoing issues would be to limit the application of the Proposed Rule to a registrant’s PEO and PFO, which would be consistent with the unique status of those executive positions. The PEO and PFO positions are the sole positions named by title for which pay information must be disclosed in a registrant’s proxy.[6] Sarbanes-Oxley certification requirements solely apply to a registrant’s PEO and PFO.[7] Generally, the PFO is the chief spokesperson for a registrant on all financial matters and is the executive officer along with the PEO who holds periodic calls with market analysts and institutional shareholders to discuss the registrant’s financial condition, business strategy and prospects. Simply, PEOs and PFOs are the face of registrants unlike any other executive officer position and, as such, their compensation receives the greatest scrutiny from shareholders.

The benefits of limiting the Proposed Rule to a registrant’s PEO and PFO would include the following:

-

-

-

- Enhanced ease for investors to discern the relationship between a PFO’s compensation and registrant performance (which would not be the case with respect to using Average NEO Compensation).

- Enhanced comparability of disclosures across covered years for a registrant and across registrants.

- Reduced burden in producing the required disclosure[8].

- Reduced scope and complexity of explanatory and/or volitional disclosures that would have otherwise been necessary to explain the relationship between Average NEO Compensation and registrant performance.

-

-

Base the amount “actually paid” under a stock option grant on the option’s in-the-money value on the date of vesting.

For the reasons discussed below, we are recommending that the Commission revise the Proposed Rule to provide that the determination of amounts actually paid under a stock option would be based on the vesting date in-the-money value of the option.

Under the Proposed Rule, a registrant would be required to determine compensation actually paid to each individual named executive officer for each covered year. For the most part, this determination would be straightforward and transparent to investors. For example, cash compensation actually paid to a named executive officer would be based directly on amounts disclosed in a registrant’s Summary Compensation Table without adjustment (e.g., disclosures relating to base salary, bonus, non-equity incentive plan compensation). Similarly, compensation actually paid to a named executive officer under a stock award[9] that vested during a covered year would be based directly on amounts disclosed in a registrant’s Option Exercises and Stock Vested Table. Such amounts would be equal to an award’s face value on the date of vesting (i.e., the number of shares subject to the stock award multiplied by the registrant’s share price on the date of vesting). The foregoing approach to determine amounts actually paid to a named executive officer is reasonable and consistent with the intent of the Dodd-Frank Act.

Under the Proposed Rule, amounts actually paid under a stock option would be based on the option’s vesting date “fair value.” Fair value would be based on a theoretical value (not on an observable market value) derived under a mathematical model that meets the requirements of ASC Topic 718, such as the Black-Scholes-Merton option pricing model. This theoretical value may be greater than or less than the value that could be derived from the exercise of an option on the date of vesting. Similarly, this theoretical value may differ materially from the actual value derived from the option’s exercise at a future date. In all cases, it would be mere coincidence for the theoretical value to equal the actual value derived upon the option’s exercise. Clearly, an option’s theoretical value would not be reasonably representative of amounts that may be or could be actually paid under the option. Therefore, the use of such theoretical value would distort the relationship between compensation actually paid and registrant performance. The Dodd-Frank mandate is clear that the Pay versus Performance Disclosure must relate to amounts “actually paid” to a registrant’s executive. The Commission’s proposed treatment of stock options simply does not meet this mandate.

To meet the mandate of Dodd-Frank, we recommend that the Commission revise the Proposed Rule to treat stock options in the same manner as stock awards. That is, the determination of compensation actually paid under a stock option would be based on an observable market value on the date of vesting (i.e., the spread value) and would not take into account potential post-vesting changes in such market value. Under this approach, in cases where an option was in-the-money on the date of vesting, amounts actually paid under the option would be equal to this in-the-money value. However, in cases where an option is at-the-money or out-of-the-money on the date of vesting, amounts actually paid under such an option would be equal to zero.

The benefits of the foregoing approach to valuing stock options would include the following:

-

-

-

-

-

-

- The valuation method would be transparent and easily understood by investors.

- The burden of valuing options would be substantially reduced[10].

- The comparability of option valuations would be greatly enhanced for covered years for a registrant and across registrants.

-

-

-

-

-

Eliminate (or in the alternative modify) the disclosure of peer group TSR.

For the reasons discussed below, we are recommending that the Commission revise the Proposed Rule to either eliminate or, in the alternative, modify the requirement that registrants disclose peer group TSR.

The Proposed Rule would require a registrant to disclose TSR (weighted by market cap) of a registrant-selected peer group for each covered year. In the Release, the Commission claims that the “disclosure about the relationship between registrant TSR and peer group TSR would provide information that investors can use to compare a registrant’s performance with that of its peers.” [11] The Commission further claims that such disclosure “may provide a useful point of comparison to assess the relationship between the registrant’s executive compensation actually paid and its financial performance compared to the performance of its peers during the same time period.”[12]

In principle, we agree with the Commission that the Pay for Performance Disclosure could potentially be enhanced through the disclosure of any number of additional data points, including the disclosure of data on peer group TSR. However, the issue presented by the Proposed Rule is not the merits of disclosing peer group TSR, but whether it is called for under the Dodd-Frank Act. The express mandate of the Dodd-Frank Act is clearly limited to the disclosure of the relationship between compensation actually paid to executives and registrant performance. The language of the statute is not ambiguous on this matter. Further, neither the legislative history of the Dodd-Frank Act nor the context within the overall statutory scheme suggests that Congress intended this mandate to cover the relationship between a registrant’s TSR and peer group TSR. In fact, the Commission has never previously interpreted any disclosure mandates on executive compensation to require disclosure of information or data not directly related to the registrant. We believe the Commission has no reasonable basis to expand the disclosure mandate under the Dodd-Frank Act to include the disclosure of peer group TSR. Accordingly, the Proposed Rule should be revised to exclude such disclosure requirement.

However, if the Commission’s final rule should retain the peer group TSR disclosure requirement, we recommend a modification in the method used to determine peer group TSR. Under the Proposed Rule, peer group TSR would be weighted according to each peer company’s market capitalization. This approach is inconsistent with the manner in which registrants typically determine peer group TSR used in performance plans. The overwhelming market practice of registrants is to use unweighted average peer group TSR (not market cap weighted TSR) in TSR-based performance plans. Further, the proposed use of market cap weighted TSR could substantially skew disclosed TSR data based on the share price movement of one or two peer companies with market caps much larger than other companies within the peer group, which likely may be the top performers among the peer group. For these reasons, we recommend that the Commission revise the Proposed Rule to provide that peer group TSR be determined on an unweighted basis, if peer group TSR is required to be disclosed under the Commission’s final rule.

We believe that our recommended revisions to the Proposed Rule would facilitate an investor’s understanding of the relationship between executive pay and registrant performance and substantially simplify and shorten the disclosure.

We have attached to our comment letter an illustrative example of the recommended graphical disclosure (including an introductory paragraph) based on an unnamed registrant’s proxy-disclosed compensation data on its PEO.

We appreciate the opportunity the Commission has afforded the public to comment on its proposed rule implementing Section 953(a) of the Dodd-Frank Act. We welcome the opportunity to discuss with the Commission and its staff our comments provided herein.

Sincerely,

Meridian Compensation Partners, LLC

Donald G. Kalfen

Partner

* * * * * *

[1] Release at p. 20.

[2] Release at p. 26.

[3] Average NEO Compensation would be based on the compensation actually paid to a registrant’s PFO and the three highest paid executive officers other than the PFO and PEO. Id.

[4] Release at p. 28.

[5] Id.

[6] Item 402(a)(3)(i) and (ii) of Regulation S-K.

[7] A registrant’s PEO and PFO are required to file with the Commission certain certification relating to the registrant’s financial controls and financial statements pursuant to Sections 302 and 906 of the Sarbanes-Oxley Act.

[8] See discussion in section immediately below regarding burden of calculating vesting date fair value of stock option grants.

[9] Stock award refers to full-value awards such as restricted stock, restricted stock units and performance shares.

[10] The valuation of options under Black-Scholes or other mathematical models would be particularly burdensome where a registrant frequently grants stock options to its named executive officers. For example, an option that vests ratably over 4 years would have 4 separate tranches each of which would need to be valued on the date vesting. The number of tranches subject to valuation would substantially increase if such an option was granted annually to each named executive officer. In such a case, a registrant would be required to determine the fair value of tranches vesting under 4 separate option grants (i.e., option grants made over the prior 4 years) across 5 covered years. This would translate into 20 option tranches, each of which would require a separate valuation on their respective vesting dates. In addition to creating an administrative burden, companies that lack the internal capabilities to perform such valuations would be required to engage and pay third parties to perform the valuations.

[11] Release at p. 19.

[12] Id.