On November 6, 2014, Institutional Shareholder Services (ISS) issued final updates to its proxy voting policies that included a complete overhaul of its policies on equity plan proposals (see Meridian Client Update dated November 10, 2014). At the end of last year, ISS issued significant guidance in the form of FAQs on its new voting policies with regard to equity plan proposals. This Client Update provides a summary and commentary on this latest guidance.

Overview of New Policy on Equity Plan Proposals

ISS has implemented new proxy voting guidelines applicable to equity plan proposals included in 2015 proxies. Under these guidelines (referred to as the “Equity Plan Scorecard”), ISS will determine its vote recommendation on such proposals based on the outcome of the following three-part analysis: (i) plan cost, (ii) plan features and (iii) company grant practices. ISS will employ separate scoring models for equity plan proposals from S&P 500, Russell 3000 (excluding S&P 500), Non-Russell 3000 companies and recent IPO/bankruptcy emergent companies. This analysis will yield a specific point score up to a maximum score of 100. Generally, ISS will issue a positive vote recommendation if a company’s point score is at least 53.

ISS designed the Equity Plan Scorecard so that a “positive” factor may act to mitigate the presence of a “negative” factor. For example, the presence of favorable plan features (e.g., minimum vesting standards, no liberal share recycling, double-trigger vesting of equity awards in connection with a change in control) may mitigate ISS concerns regarding excessive equity plan costs or burn rate. Conversely, if ISS identifies provisions that are problematic, ISS might recommend voting AGAINST an equity plan proposal, irrespective of whether the cost of the equity plan meets ISS policy requirements.

The Real Story Behind the Equity Plan Scorecard and ISS’s Scoring Methodology

The Equity Plan Scorecard scoring methodology underlies (and obfuscates to a degree) the real upshot in ISS’s new proxy voting policies on equity plan proposals. That is, the size of a permissible share pool is now a fluid concept rather than a fixed one as was the case under ISS’s prior policy. Through essentially a “carrot and stick” approach, ISS will increase the size of a permissible share pool to the extent a company and its equity plan complies with ISS’s proxy voting policies.

For example, we have seen where a company has agreed to revise an equity plan to include certain favorable plan features (e.g., minimum vesting standards), ISS has increased by 25% the size of the allowable share pool. Conversely, to induce companies to reduce the size of the requested share pool, ISS assigns a higher point score to a requested share pool with a cost that is not greater than 65% of the ISS-determined cost benchmark.

Companies will now have to wrestle with multiple scenarios to determine the proper balance between the ISS allowable share pool and the desired plan features (as well as certain other practices). As always, we stress that corporate boards and compensation committees have a fiduciary obligation to approve plan designs and share pools that are in the best interest of shareholders and their company, irrespective of whether such design and share pools meet ISS’s proxy voting policies.

Balanced Scorecard Categories, Factors and Weighting

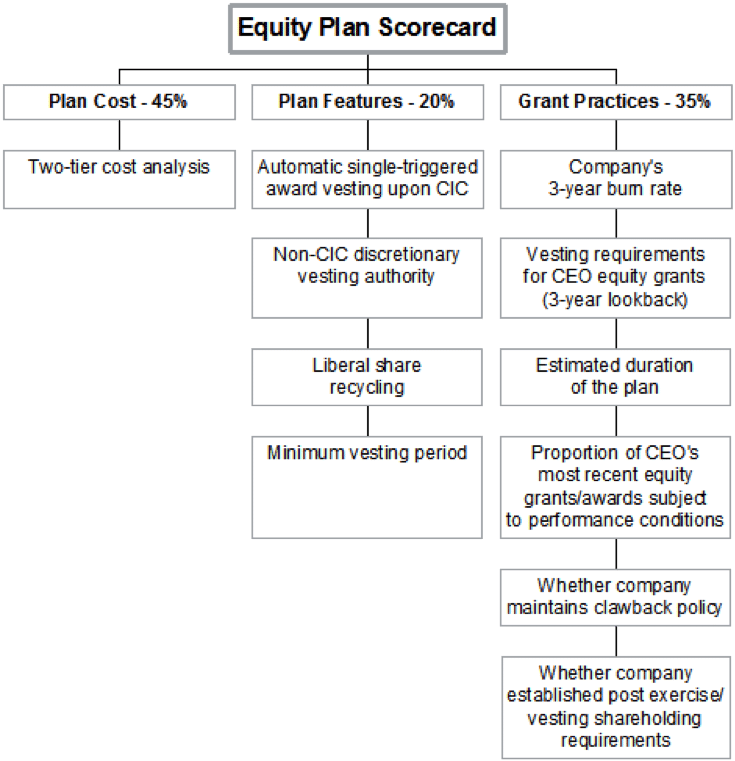

The diagram below shows the factors ISS will consider under each category of the Equity Plan Scorecard (“EPSC”) when evaluating an equity plan proposal and the weight assigned to each category for S&P 500 and Russell 3000 companies.

An equity proposal may receive up to 100 points under the EPSC. For Russell 3000 and S&P 500 companies, the following is the maximum point score by category: 45 points for the plan costs, 20 points for the plan features and 35 points for grant practices. ISS has not disclosed maximum point score by individual factor. A score of 53 points or higher will generally result in ISS recommending FOR an equity plan proposal.

ISS analysis under the Grant Practices category will not apply to companies that have emerged from bankruptcy or have had an initial public offering within the prior three fiscal years. For those companies, the Plan Cost category is weighted 60% and the Plan Features category is weighted 40%. For non-Russell 3000 companies, the Plan Cost category is weighted 45%, the Plan Features category is weighted 30% and the Grant Practices category (only the burn rate and plan duration factors are applicable) is weighted 25%.

Special Circumstances Resulting in a Negative Vote Recommendation

Generally, the following equity plan features will likely result in ISS recommending AGAINST a company’s equity plan proposal, regardless of a company’s EPSC point total:

- The equity plan provides for the vesting/settlement of equity awards upon a “liberal change-of-control” event (i.e., where a change in control may be triggered without consummation of the underlying transaction) with no requirement that the award holder terminate employment,

- The equity plan permits repricing or cash buyout of underwater options without shareholder approval (either by expressly permitting it—for NYSE and Nasdaq listed companies—or by not prohibiting it when the company has a history of repricing—for companies that are not listed on a stock exchange),

- The equity plan is a vehicle for problematic pay practices (i.e., the plan guarantees equity awards to executives or provides for a tax gross-up on equity awards),

- The equity plan is a vehicle for a CEO pay-for-performance disconnect (historically, ISS has rarely found that an equity plan was a vehicle for a CEO pay-for-performance disconnect (approximately ½ of 1% of the time)), or

- The equity plan includes other features that have a significant negative impact on shareholder interests (as determined by ISS).

Explanation of Category Factors

ISS’s new policy on equity plan proposals and the recently issued FAQs provide the following guidance on the indicated category factors.

Plan Cost

ISS will determine two separate plan “costs” under its proprietary cost model (i.e., shareholder value transfer (SVT) model) as follows:

- Tier 1 Cost. An equity plan’s Tier 1 cost is based on shares subject to shareholder approval (“A shares”) plus all shares that remain available for issuance (“B shares”) plus shares related to unexercised/unvested outstanding awards (“C shares”).

- Tier 2 Cost. An equity plan’s Tier 2 cost is based only A shares and B shares, excluding C shares.

ISS will evaluate an equity plan’s Tier 1 costs and Tier 2 costs against ISS-determined cost benchmark. ISS’s proprietary SVT model determines SVT benchmark costs (expressed as a percentage of the company’s market capitalization) based on regression analysis that take into account a company’s market cap, industry, and performance indicators with the strongest correlation to industry TSR performance. The SVT model also will take into account shares available under a non-employee director plan. Equity plans with plan costs at or below 65% of the ISS-determined cost benchmark will receive the maximum points for this factor.

Plan Features

ISS has provided the following guidance on the factors under the Plan Features category.

- Liberal share recycling. Liberal share recycling covers plan provisions that allow shares to return to the share pool to be available for future grants in the following circumstances: (i) shares that are withheld by a company or tendered by an employee to pay the exercise price of an option, (ii) shares withheld by the company or tendered by an employee to satisfy tax withholding obligations associated with any type of equity award, (iii) shares subject to a stock appreciation right that were not issued upon the exercise of such stock appreciation right and (iv) shares purchased on the open market with the proceeds from the exercise of a stock option. Equity plans that prohibit share recycling will receive the maximum points for this factor.

- Minimum vesting standard. ISS defines “minimum vesting period” to be at least one year in duration. This minimum vesting period must be applicable to all types of equity awards. An equity plan may provide that upon a change in control or due to a participant’s death or disability the minimum vesting period will be automatically waived and truncated. Automatic acceleration for any other reason (e.g., retirement, involuntary termination without cause) would not comply with this factor. We have obtained informal advice from ISS that a company may exclude up to 5% of an equity plan’s share pool from the minimum vesting standards. Equity plans that meet the minimum vesting standard will receive the maximum points for this factor.

- Non-CIC discretionary vesting authority. Generally, a Company’s EPSC score will be adversely impacted if the administrator of the company’s equity plan retains broad discretionary authority to accelerate the vesting of an outstanding equity award. According to informal advice obtained from ISS, this will be true even if the plan administrator may not exercise such discretion until after a participant completes a year of service. However, if a plan administrator’s discretionary authority is limited to accelerating vesting solely upon a change in control or due to a participant’s death or disability, ISS will assign the maximum points for this factor.

- Single-trigger vesting of equity awards. This factor relates to plan provisions that require the automatic vesting of equity awards solely upon a change in control (“Single-Trigger Vesting”). ISS will assign no points for this factor if an equity plan includes Single-Trigger Vesting of equity awards and will assign maximum points if an equity plan does not include Single-Trigger Vesting. ISS does not expressly state the type of alternative vesting triggers that would yield a maximum point score. However, at a minimum, we believe that ISS will assign maximum point score for equity plans that subject awards to double-trigger vesting (i.e., vesting upon a qualifying termination of employment following a change in control). Based on informal guidance from ISS, we also believe the following types of vesting triggers would also yield the maximum points for this factor: (i) vesting at the discretion of the plan administrator and (ii) vesting upon a change in control if the successor entity fails to assume or replace outstanding equity awards.

Grant Practices

ISS has provided the following guidance on the factors under the Plan Features category.

- Three-year burn rate. ISS will assess a company’s three-year average burn rate against two benchmarks: (i) 4-digit GICS industry group’s 3-year industry group burn rate plus one standard deviation and (iii) 2 percent de minimis burn rate. ISS will determine separate mean burn rates for the following indices: (i) S&P 500 companies, (ii) Russell 3000 companies (exclusive of S&P 500 companies) and (iii) Non-Russell 3000 companies. In contrast to ISS’s prior policy that permitted a company to mitigate a failed burn rate test by making a prospective burn rate commitment, the new policy will not allow for such mitigation. Equity plans with a burn rate at or below 50% of the applicable benchmark will receive the maximum points for this factor.

- Duration of plan. ISS will determine the estimated duration of an equity plan by dividing the sum of shares remaining available for future grants and the new shares requested by a company’s three-year average burn rate. If a company’s proposed equity plan has a fungible share design (where full-value awards count against the share reserve at a higher rate than options/SARs), the proportion of the burn rate shares that are full-value awards will be multiplied by that fungible ratio in order to estimate the plan’s duration. Equity plans with an estimated duration of no more than five years will receive the maximum points for this factor.

- Vesting standards in CEO equity grants. ISS will evaluate the vesting standards in the most recent equity grants made to the CEO within the prior three years. Equity plans with vesting period of greater than four years will receive the maximum points for this factor.

- CEO proportion of performance-based awards. ISS will evaluate the proportion of the CEO’s most recent fiscal year equity awards that are conditioned on achievement of a disclosed performance goal or goals. The proportion of the CEO’s equity grants deemed to be “performance conditioned” is based on the ISS valuation of awards reported in a company’s Grants of Plan-Based Awards table. ISS does not consider time-vested options and SARs performance-based awards. However, ISS will treat options and SARs as performance-based awards if either vesting or value received is conditioned upon the attainment of a specified performance goal or goals or the exercise price is at a substantial and meaningful premium over the grant date share price. If at least 50% of the CEO’s equity awards are performance-based, ISS will assign the maximum points for this factor.

- Clawback policy. ISS will evaluate whether a company has a policy that would authorize recovery of gains from all or most equity awards in the event of certain financial restatements. If a company maintains a disclosed clawback policy, ISS will assign the maximum points for this factor.

- Holding period. ISS will evaluate whether a company requires employees to hold shares received upon the exercise or settlement of equity grants for a specified period. If a company maintains a disclosed share holding policy of at least one year, ISS assigns the maximum points for this factor. If a company maintains a “hold until ownership guidelines are met” requirement, then ISS will assign ½ of the full points for this factor.

Attached to this Client Update is a comprehensive summary of the EPSC scoring methodology for each factor.

Summary of EPSC Scoring Methodology

| Factor | Definition | Scoring Basis | |

| Plan Cost | Tier 1 costs | Tier 1 cost relative to peers based on new shares requested, shares available under existing plans and shares subject to existing awards | Plan cost at or below 65% of benchmark – full points

Plan cost in excess of 65% of benchmark – partial to zero points |

| Tier 2 costs | Tier 2 cost relative to peers based on new shares requested and shares available under existing plans | Plan cost at or below 65% of benchmark – full points

Plan cost in excess of 65% of benchmark – partial to zero points |

|

| Plan Features | CIC Single Trigger | Does the plan provide for immediate vesting of equity awards upon a CIC? | Yes – no points

No – full points |

| Liberal Share Recycling (Full-value awards) | Does the plan permit liberal share recycling? | Yes – no points

No – full points |

|

| Liberal Share Recycling (Options/SARs) | Does the plan permit liberal share recycling? | Yes – no points

No – full points |

|

| Minimum Vesting Requirement | Does the plan stipulate a minimum vesting period of at least one year for any award? | No – no points

Yes – full points |

|

| Discretion to Accelerate Vesting | Does the plan grant the plan administrator the authority to accelerate vesting of an award (unrelated to a CIC, death or disability)? | Yes – no points

No – full points |

|

| 3-Year Average Burn Rate | Does the company’s 3-year average burn rate exceed industry/index benchmark and de minimis burn rate cap? | Burn rate is at or below 50% of benchmark – full points

Burn rate over 50% of benchmark – partial to zero points |

|

| Grant Practices | Estimated Plan Duration | What is the estimated duration of the proposed share reserve (new shares plus existing reserve)? | =/< 5 years – full points

>5 </= 6 years – ½ of full points Greater than 6 years – no points |

| CEO’s Grant Vesting Period | What is the vesting period for the most recent fiscal year equity awards granted to the CEO? | > 4 years – full points

=/> 3 years </= 4 – ½ of full points Less than 3 years – no points |

|

| CEO’s Proportion of Performance- Conditioned Awards | What portion of the CEO’s most recent fiscal year equity awards conditioned on the achievement of one more disclosed performance goals? | 50% or more – full points

33% < 50% — ½ of full points Less than 33% – no points |

|

| Clawback Policy | Does the company have a policy that would authorize recovery of gains from all or most equity awards in the event of certain financial restatements? | Yes – full points

No – no points |

|

| Holding Period | What period must employees hold shares received upon the exercise or settlement of equity grants? | At least 12 months – full points

To end of employment – full points Less than 12 months – ½ of full points Until ownership requirements met – ½ full points No share holding requirement – no points |

* * * * *

The Client Update is prepared by Meridian Compensation Partners’ Technical Team led by Donald Kalfen. Questions regarding this Client Update or executive compensation technical issues may be directed to Donald Kalfen at 847-235-3605 or dkalfen@meridiancp.com.

This report is a publication of Meridian Compensation Partners, LLC, provides general information for reference purposes only, and should not be construed as legal or accounting advice or a legal or accounting opinion on any specific fact or circumstances. The information provided herein should be reviewed with appropriate advisers concerning your own situation and issues.

Meridian comment. The full implications of ISS’s EPSC will become clearer as we move through this proxy season. However, what is clear now is that EPSC is an over-engineered and complex methodology for evaluating the merits of a company’s equity plan proposal. ISS has presented no empirical or philosophical bases that suggest a correlation should exist between the allowable size of an equity plan’s share pool and plan features and grant practices, but complex models can encourage use of ISS’s consulting services for equity plan proposals.

The manner in which ISS makes its vote recommendations on equity plan proposals as well as on other proxy proposals may become subject to close scrutiny by the Securities and Exchange Commission (“SEC”). The SEC recently released its examination priorities for 2015 that included a review of proxy service providers. Specifically, the SEC indicated that it “will examine select proxy advisory service firms, including how they make recommendations on proxy voting and how they disclose and mitigate potential conflicts of interest. In concert with this examination, the SEC will also “examine investment advisers’ compliance with their fiduciary duty in voting proxies on behalf of investors.” We will be closely monitoring and reporting on SEC activity in this area.