First and foremost, we hope you, your families and your colleagues are staying safe and healthy during this global health crisis. We appreciate normal business operations for many companies have been upended due to the COVID-19 pandemic. Only through the extraordinary efforts of employees, executives and boards will companies be able to manage through the social and economic upheaval brought on by the pandemic.

For our part, Meridian is ensuring the safety and well-being of our partners and associates by requiring all to work remotely. However, during this time of sheltering-in-place, Meridian is fully operational and continues to serve the needs of our clients.

We appreciate that given the current circumstances executive compensation issues may not be top-of- mind at your organization nor do we suggest they should be. We offer this Client Update for your consideration at a time that is appropriate for you and your organization.

COVID-19 Impact on Executive Compensation

Corporate Boards and senior management teams face unprecedented challenges to govern and manage through the demand shock and substantial market downturn caused by the COVID-19 pandemic. We also understand that some industries face more serious and fundamental challenges than others. After companies address the immediate business implications, they will eventually need to address a range of governance, design and administration challenges that involve executive and non-employee director compensation programs.

This Client Update discusses considered approaches to address issues raised by the disruptive effects of COVID-19 in the following areas:

■ Corporate governance,

■ Base salary,

■ Performance-based compensation,

■ Time-based equity awards,

■ Share usage,

■ Sizing equity awards,

■ Equity pay mix, and

■ Non-employee director compensation.

Given the fast changing dynamic of this crisis, this is the first in a series of Client Updates that will monitor market practices and provide an in-depth analysis of each of these areas.

Corporate Governance

As business strategies change in response to the current health and economic crisis, issues cascade to all board committees, including the compensation committee. The situation may require compensation committees to be even more flexible, adaptable and creative than in recent years.

Compensation committees should develop guiding principles to inform their near-term decision making on these issues. These guiding principles might include the following:

■ Consider and, if necessary, modify long-held philosophies and policies.

■ Consider non-conventional program designs, if necessary, to keep management and employees motivated, engaged and aligned with current and rapidly changing business strategies.

■ Understand proxy advisory firm perspectives but not let their strict guidelines restrict or limit the compensation committee from taking actions appropriate for their organizations. Proxy advisory firm guidelines may likewise evolve in response to the current circumstances.

■ Consider how executives should share in the compensation burdens born by other employees across the organization.

■ Consider the impact on all company stakeholders, including employees, shareholders, supply chain members, consumers and communities in which the company has an interest.

While it may be too soon to make any decisions or take action concerning 2020 pay for most companies, there are steps companies may consider, including:

■ If the 2020 proxy has not been filed, add the following disclosure: (i) the proxy relates to 2019 performance and compensation, neither of which were affected by the COVID-19 pandemic, (ii) the COVID-19 pandemic could significantly impact 2020 financial results and compensation outcomes and (iii) the specific actions taken by the board and executives to address the effect of the COVID-19 pandemic on business operations.

■ Share guiding principles with management to ensure continued motivation and common expectations. Develop a cadence of information sharing both on business impact and potential compensation implications throughout the year.

■ Engage shareholders to discuss and obtain feedback on significant changes in compensation program design.

Base Salary

Certain industrial sectors have shored up their liquidity through salary decreases or headcount reductions. In some cases, top executives have volunteered salary reductions or extended salary abstentions as important demonstrations of solidarity with impacted employees.

More than 30 major public companies to date have disclosed executive salary reductions. Over one-half of these companies are either in the airline or hospitality industries (e.g., United Airlines, Delta, Marriot International, Norwegian Cruise Line, Hyatt Hotels). In other situations, companies have delayed or rescinded previously approved salary increases for management and employees. Compensation committees and management should note that unless specifically addressed, reductions in base salary may directly affect other pay elements and protections (e.g., bonus determination, severance calculations, retirement benefits, life and disability insurance coverage).

Performance-Based Compensation

Reduced commercial activity will have the greatest impact on both short- and long-term performance- based compensation. In most instances, outstanding business plans and performance goals have been rendered challenging or obsolete, and companies have no current certainty about the timing or pace of a recovery to restate their plans with confidence. Situations differ across industries and companies, and therefore the considered actions cross a range of potential responses described below.

Potential Strategies for Outstanding Short- and Long-Term Incentive Awards (where performance metrics and goals have been set)

■ Maintain status quo and take a wait and see attitude until later this year (given the current uncertainty, any changes made now could become quickly obsolete, so we suggest considering a “reflection” period mid-year once companies have a better sense of the crisis and its impact on business).

■ Exercise greater discretion in cash/long-term incentive outcomes to consider the impact of COVID-19 on prescribed metrics, or even the affordability of a bonus altogether despite certain metric achievements. (We believe most companies expect to exercise more discretion than usual in 2020 outcomes.)

■ Modify existing performance goals to reflect COVID-19’s anticipated effects on financial performance (this situation would require reasonable certainty about the extent and impact on financial results, which seems unlikely under current circumstances but could be possible later this year, also this could raise accounting issues).

■ Eliminate incentive opportunity for 2020 (while a drastic action, we have seen top officers at certain companies, agree to forego bonus payouts for the current year, and in some cases companies already acknowledge they will not pay a 2020 bonus).

For outstanding performance-based equity awards subject to a market condition (e.g., absolute and/or relative total shareholder return), generally compensation committees are not currently contemplating any modifications to those awards, despite substantial market declines. However, companies should consider whether to cap payouts at no more than target if negative TSR would result in a payout.

Potential Strategies for Short- and Long-Term Incentive Awards (where performance metrics have not yet been set)

■ Short-term incentive awards

― Allow for end-of-performance period adjustments to earned awards (by calculation or discretion) to take into account the impact of COVID-19 on financial performance (mitigates the need to set performance goals that accurately predict COVID-19’s impact on financial performance).

― Incorporate discretion into the determination of incentive award payouts (given ongoing uncertainties about the economic impact of COVID-19, some companies that continue to pay a 2020 bonus may resort to a discretionary evaluation for all award payouts to use hindsight to appropriately reward management’s efforts and accomplishments).

― Allocate a portion (e.g., 25% or more) of the incentive awards to the achievement of important strategic, operational and individual objectives not directly tied to financial performance (this can mitigate the adverse effects of COVID-19, if desired).

― Consider shifts from business unit to corporate-wide goals and/or elimination of individual performance goals this year (encourages team approach to addressing critical business issues during the pandemic crisis).

■ Performance-based long-term incentive awards

― Delay the grant until economic conditions settle (may prove difficult to determine optimal timing of a grant and would upset normal grant practices/commitments; most companies may still grant time- based long-term incentive awards in accordance with a company’s normal grant practices, with or without a reduction in grant value to reflect current price-see discussion below).

― Establish shorter performance periods within a new long-term incentive award (e.g., 3 one-year periods, 3-year service period with a 1-year performance period) (may ease the development of appropriate performance goals; however, not preferred by proxy advisory firms).

― Include a qualitative component (in conjunction with a financial metric) to allow for more holistic assessment of performance (e.g. 50% TSR, 50% Strategic Performance) (this approach can permit greater committee judgement in the performance evaluation, but also create adverse accounting outcomes).

― Provide language in award agreements for an end-of-period adjustment to earned long-term incentive awards to take into account the impact of COVID-19 on financial performance (may ease development of long-term performance metrics and goals, but requires some certainty to distinguish and measure the ultimate impact; could also result in adverse accounting consequences).

― Incorporate a relative total shareholder return metric (allows the market to measure the effects of COVID-19 on share price and eliminates the need to adjust performance metrics to identify the extent of COVID-19 effects on financial performance; however, award remains subject to volatile equity markets).

― Grant only time-based restricted stock/units based on an evaluation of prior year performance and market competitive compensation levels (avoids the need to determine appropriate performance metrics, but has potentially adverse shareholder and advisory group optics).

Time-Based Long-Term Incentive Awards

For time-based long-term incentive awards, such as stock options and time-based restricted stock/unit awards, compensation committees appear headed to maintain the status quo. For myriad reasons and despite the plunge in share price rendering many stock option awards deeply underwater, large cap companies are not likely to consider “repricing” such awards or exchanging those awards for full value grants or cash at this time.

Sizing Equity Awards/Share Usage

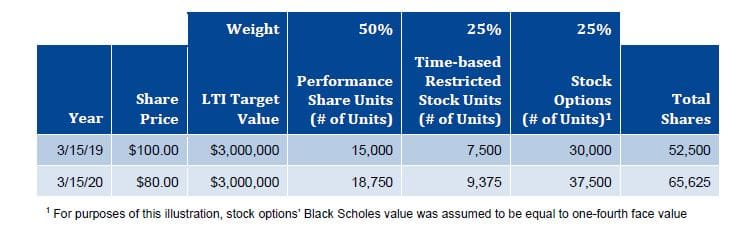

We expect companies that have yet to grant their 2020 equity awards to consider the impact of lower stock prices in equity grant sizes. Lower share prices require more shares to deliver comparable grant- date value, as illustrated below.

From the observed ranges of stock price decreases in 2020, companies may need from 20% to over 300% more shares to deliver comparable LTI value in a current (or future) grant.

Most calendar-year companies made their awards prior to the precipitous share price decline. However, for those that make their grants later in the year, share usage will increase considerably. This could put a significant strain on share availability and reduce the life of the current share pool. In certain instances, current share pool levels might be insufficient to fully fund regular annual LTI grant levels. In addition, high share usage may create excessive dilution and leverage, resulting in realized compensation that is not aligned with shareholder experience, particularly if the recovery is faster than anticipated.

Managing share usage

To reduce the potential strain on share pool levels, companies could choose to settle some or all equity awards in cash. However, liquidity concerns may make share monetization impractical. Without committing to either share or cash settlement, compensation committees could consider the following actions:

■ Provide for the settlement of future awards in cash, shares or a combination of both at the discretion of the compensation committee (this would allow, but not require, the compensation committee to manage the drawdown of the share pool and use of cash without the need to modify overall design and economics of prior equity grants).

■ Modify existing awards to settle currently outstanding equity awards in cash, shares or a combination of both at this discretion of the compensation committee (this would allow the compensation committee to further manage the drawdown of the share pool).

As an alternative to settling future awards in cash, a company could grant long-term cash performance units rather than equity shares to decrease share usage. However, this approach has a higher risk of generating compensation outcomes that are not aligned with shareholder experience.

Sizing equity awards

To address sizing issues, compensation committees have considered the following actions:

■ Maintain status quo grant practices where share pool is large enough to at least fund a full year of anticipated equity grants and where the annual “burn rate” is reasonable in relation to the company’s long-term average.

■ Use a higher trailing average share price over the most recent 30, 60 or 90 trading days to size awards.

■ Chose an “arbitrary” level of reduction in the dollar value of equity awards – e.g., a reduction of 10% or more in the grant date award value.

■ Limit grants to the same number of shares that the company awarded in the most recent previous award cycle.

■ Set a floor stock price to be used for determining shares.

■ Set an annual dilution cap and prorate planned awards as needed to stay below the cap.

Equity Pay Mix

Given economic and equity market uncertainties, compensation committees, especially at those companies that have yet to make awards for 2020, may need take a fresh look at the mix of LTI awards and consider the following:

■ Maintain the status quo.

■ Simplify equity pay mix by moving to one equity vehicle, (likely restricted shares).

■ Eliminate performance-based equity awards in favor of more time-based restricted stock/unit awards or cash-denominated performance awards (this action would be viewed negatively by the proxy advisory firms and some institutional shareholders).

Non-Employee Director Compensation

In certain recently announced executive pay actions, we have observed that some boards are making parallel changes to their own compensation, including:

■ Elimination or reduction of cash retainers,

■ Rescission of previously approved director fee increases.

Many companies face large stock price differences between early-year employee stock grants and upcoming director grants planned for the annual shareholder meeting. We have observed that some boards, particularly in industries seriously impacted by COVID-19, may elect to reduce their director grants by a specific percentage, or apply the same price used to size employee equity.

We will continue to closely monitor and report on developments relating to approaches companies and compensation committees have considered or implemented to address COVID-19 issues affecting their executive and non-employee director compensation programs.

* * * * *

The Client Update is prepared by Meridian Compensation Partners’ Governance and Regulatory Team led by Donald Kalfen. Questions regarding this Client Update or executive compensation technical issues may be directed to Donald Kalfen at 847-235- 3605 or dkalfen@meridiancp.com.

This report is a publication of Meridian Compensation Partners, LLC, provides general information for reference purposes only, and should not be construed as legal or accounting advice or a legal or accounting opinion on any specific facts or circumstances. The information provided herein should be reviewed with appropriate advisors concerning your own situation and issues.

www.meridiancp.com