Requirements of Gender Diversity Law

The law’s requirements will be phased-in over a multi-year period, with compliance initially required by the close of the 2019 calendar year. A public company found to be in noncompliance with the gender diversity requirements may be subject to monetary fines. The law’s requirements are detailed below.

■ Subject Corporations. The law is solely applicable to publicly held domestic or foreign corporations with outstanding shares listed on a major U.S. stock exchange and whose principal executive offices, according to the corporation’s 10-K (annual report), are located in California. Thus, the law applies to both publicly held corporations incorporated in California and those incorporated in other states or countries (i.e., foreign corporations), so long as their principal executive offices are located in California.

■ Minimum Number of Female Board Members. Subject corporations’ board of directors must include a minimum number of female board members in accordance with the following schedule:

― By the end of calendar year 2019, a subject corporation’s board of directors must include at least one female director.

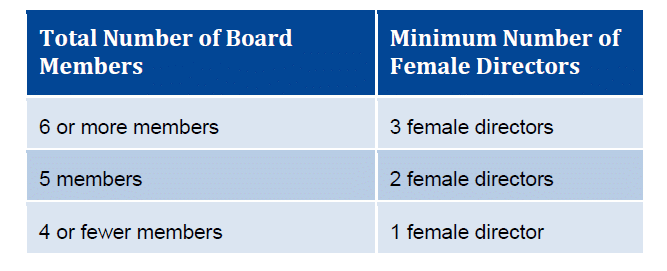

― By the end of calendar year 2021, a subject corporation’s board of directors must include the number female directors indicated in the chart below:

― The law permits a corporation to meet the foregoing gender quota by increasing the number of board members as necessary to accommodate new female directors. Under a company’s charter or bylaws, a board may (or may not) be authorized to unilaterally increase the size of the board without seeking shareholder approval.

■ Fines for Noncompliance. The law authorizes, but does not require, the California Secretary of State to impose fines for noncompliance in accordance with the following schedule:

― For a first violation, the amount of $100,000.

― For a second or subsequent violation, the amount of $300,000.

A subject corporation will be in noncompliance with the new law if a woman does not hold the required seat for at least a portion of a calendar year.

In addition, the law authorizes, but does not require, the California Secretary of State to impose a $100,000 fine on subject corporations that fail to timely report board composition (e.g., gender information).

■ Publication of Secretary of State Report. Under the law, the California Secretary of State is required to publish the following reports based on information provided by subject corporations:

― No later than July 1, 2019, the Secretary of State must publish a report on the number of domestic and foreign corporations whose principal executive offices, according to the corporation’s 10-K (annual report), are located in California and who have at least one female director.

― No later than March 1, 2020, and annually thereafter, the Secretary of State must publish a report regarding, at a minimum, all of the following:

- The number of subject corporations that were in compliance with the requirements of the law during at least one point during the preceding calendar year.

- The number of publicly held corporations that moved their United States headquarters to California from another state or out of California into another state during the preceding calendar year.

- The number of subject corporations during the preceding year that are no longer publicly traded.

Rationale for Gender Diversity Law

The preamble to the law cites two principal reasons for the law’s adoption: (i) to address the slow pace of gender diversification on publicly held corporation boards and (ii) to enhance corporate performance. According to an outside study cited in the preamble, “it will take 40 or 50 years to achieve gender parity, if something is not done proactively.” Moreover, the preamble references four independent studies that have concluded that corporate performance is enhanced when women serve on the board. As further support for the new law, the preamble notes that other countries, such as Germany, Norway, France, Spain, Iceland and the Netherlands, have addressed the lack of gender diversity on corporate boards through mandated gender quotas.

Meridian Comment

According to the preamble to the law, five states have passed resolutions calling for increased representation of women on corporate boards. However, none of these states nor any other state has pending legislation that would impose gender quotas on corporate boards. The California law may serve as a catalyst for some states to at least investigate and, perhaps ultimately pass, legislation imposing gender quotas. However, states may be apt to move slowly on this issue prior to the outcome of the inevitable legal challenges to the California law. Some legal experts have expressed doubt as to whether gender quotas would pass constitutional muster or could be lawfully imposed on corporations that are incorporated outside of California. In signing the new legislation, even Governor Brown noted the law’s potential legal deficiencies by observing that “there has been numerous objections to this bill and serious legal concerns have been raised. I don’t minimize the potential flaws that indeed may prove fatal to its ultimate implementation.”1

Position of Proxy Advisory Firms

Currently, the major proxy advisory firms’ voting policies do not include prescriptive requirements regarding female representation on corporate boards. However, Institutional Shareholder Services (ISS) has been considering this matter over the past several years, as evidenced by its annual policy surveys. We would not be surprised if ISS, within the next couple of years, updated its proxy voting policies to cover board gender diversity. Meanwhile, Glass Lewis is phasing in a voting policy on board gender diversity. Starting in 2019, Glass Lewis will generally recommend voting against the nominating committee chair of a Russell 3000 company’s board that has no female members, unless the company provides a sufficient rationale for lacking any female board members or discloses a plan to address the lack of board gender diversity. Moreover, Glass Lewis may recommend a vote against other nominating committee members depending on the size of the company, the industry in which the company operates and the governance profile of the company.

Position of Institutional Investors

Beyond individual state mandates and the voting policies of the proxy advisers, institutional shareholders loom as potentially the most influential parties on the issue of gender diversity on corporate boards. BlackRock, Vanguard, State Street and pension funds such as CalPERS and CalSTERS have called for greater board gender diversity.

■ In a 2017 letter sent to 600 companies in the United States, United Kingdom and Australia, State Street announced that it would vote against the chair of their nominating committees if there were no women directors or candidates. In keeping with this position, State Street voted against the nominating committee chair at 400 of these companies that had not initiated any efforts to increase board diversity since receiving the letter.2 Starting in 2020, State Street will vote against all members of a company’s nominating committee if a company’s board does not include any women directors.3

■ In an annual letter to CEOs, BlackRock CEO Larry Fink announced that the fund would emphasize diverse boards, as they are “less likely to succumb to groupthink or miss threats to a company’s business model.”4 Consistent with that principle, BlackRock’s 2018 proxy voting guidelines provide that the fund “would normally expect to see at least two women directors on every board.”5

■ Vanguard has not prescribed gender-based quotas, but nonetheless is a strong advocate for gender diversity. In an open letter to public company directors, Vanguard noted its position that board diversity is “an economic imperative, not an ideological choice.”6

Currently, most institutional shareholders’ proxy voting policies do not directly address diversity. We anticipate that will change over time, especially with respect to the gender composition of corporate boards as well as senior management.

* * * * *

1 Governor Brown’s Signing Statement dated September 30, 2018. Available at https://www.gov.ca.gov/wp-content/uploads/2018/09/SB-826-signing-message.pdf.

2 State Street Global Advisors press release dated November 14, 2017. Available at https://newsroom.statestreet.com/press-release/corporate/state-street-global-advisors-expands-board-diversity-guidance-companies-japa.

3 Bloomberg Law News. “State Street to Vote Against More Directors at Male-Only Boards.” September 27, 2018. Available at https://www.bloomberg.com/news/articles/2018-09-27/state-street-to-vote-against-more-directors-at-male-only-boards.

4 Letter from Larry Fink, Chair and CEO of BlackRock. Available at https://www.blackrock.com/corporate/investor-relations/larry-fink-ceo-letter.

5 BlackRock’s “Proxy Voting Guidelines for U.S. Securities”, published February 2018. Available at https://www.blackrock.com/corporate/literature/fact-sheet/blk-responsible-investment-guidelines-us.pdf.

6 Vanguard’s “open letter to directors of public companies worldwide” dated August 31, 2017. Available at https://about.vanguard.com/investment-stewardship/governance-letter-to-companies.pdf.

The Client Update is prepared by Meridian Compensation Partners’ Technical Team led by Donald Kalfen. Questions regarding this Client Update or executive compensation technical issues may be directed to Donald Kalfen at 847-235-3605 or dkalfen@meridiancp.com.

This report is a publication of Meridian Compensation Partners, LLC, provides general information for reference purposes only, and should not be construed as legal or accounting advice or a legal or accounting opinion on any specific fact or circumstances. The information provided herein should be reviewed with appropriate advisors concerning your own situation and issues.

www.meridiancp.com