On March 21, 2022, the Securities and Exchange Commission (SEC) released proposed rules that are intended to enhance and standardize climate-related disclosures.

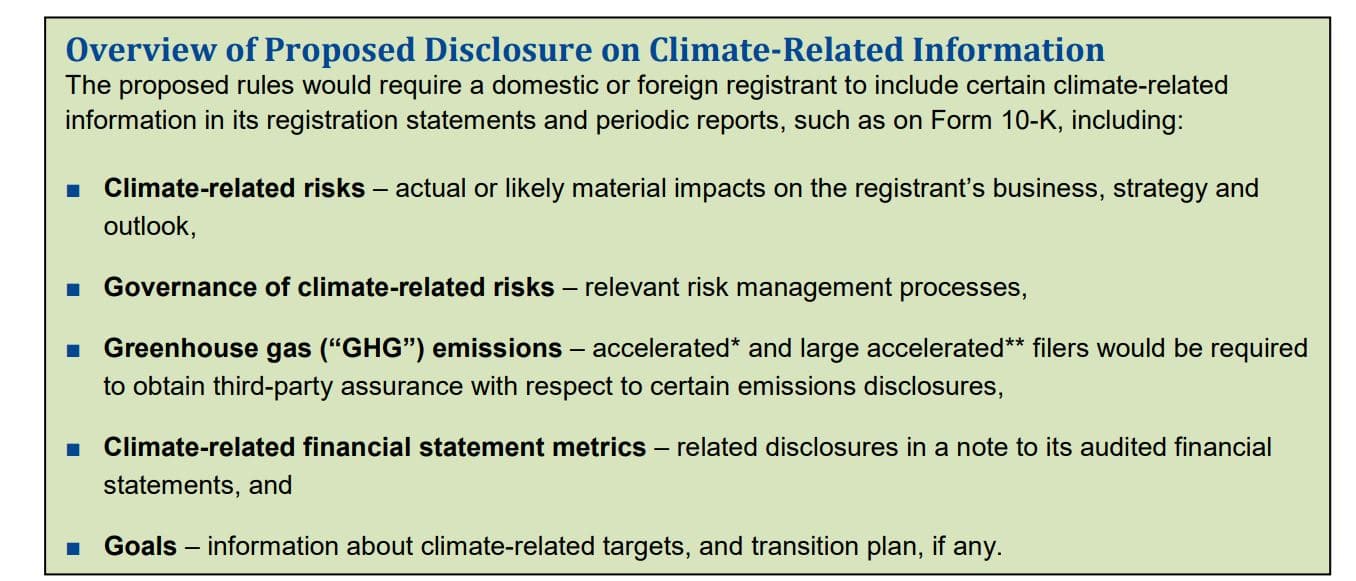

*Accelerated filers are public companies with a public float of $75 million or more but less than $700 million.

**Large accelerated filers are public companies with a public float of at least $700 million.

The SEC notes that proposed disclosures are similar to those that many companies already provide based on broadly accepted disclosure framework.

Meridian comment. While the proposed rules mandate extensive disclosures, the rules do not impose additional mandates on executive compensation disclosures.¹

The proposed rules turn on its head the SEC’s long-standing philosophy of implementing principles-based disclosures (at least for the most part), especially with respect to annual proxy disclosures. While Congress has, on occasion, directed the SEC to implement prescriptive type disclosures (e.g., DoddFrank mandates such as the CEO pay ratio disclosure), these disclosures have been limited in nature and generally not burdensome. Less than 2 years ago, the SEC modified its existing rules on describing a company’s business to clarify that public companies should disclose in their Form 10-K (annual report) information with regard to human capital management (HCM) if material to an understanding of the company’s business operations. However, this clarification was principles-based as it did not mandate or prescribe specific types or scope of HCM disclosures. Rather, each public company is empowered to determine whether and to what extent it must include such HCM disclosures in its Form 10-K.

In contrast, the proposed climate disclosure rules establish a highly prescriptive and extensive disclosure regime, which for many companies compliance will be both burdensome and expensive. Some critics have suggested the proposed rules are beyond the scope of the SEC’s rulemaking authority and are likely to face court challenges.

Content of the Proposed Disclosures

The proposed rules would require a registrant to disclose information covering a broad range of topics. The nature of these disclosures is discussed below.

Disclosure on Impact of Climate-Related Risks

■ How any climate-related risks identified by the registrant have had or are likely to have a material² impact on its business and consolidated financial statements, which may manifest over the short-, medium-, or long-term.

■ How any identified climate-related risks have affected or are likely to affect the registrant’s strategy, business model, and outlook.

■ The impact of climate-related events (severe weather events and other natural conditions) and transition activities on the line items of a registrant’s consolidated financial statements, as well as the financial estimates and assumptions used in the financial statements.

Disclosure on Transition Plans

■ If the registrant has adopted a transition plan as part of its climate-related risk management strategy, a description of the plan, including the relevant metrics and targets used to identify and manage any physical and transition risks.

Disclosures on Climate-Related Risk Management

■ Oversight and governance of climate-related risks by the registrant’s board and management.

■ Processes for identifying, assessing, and managing climate-related risks and whether any such processes are integrated into the registrant’s overall risk management system or processes.

■ If the registrant uses scenario analysis to assess the resilience of its business strategy to climate related risks, a description of the scenarios used, as well as the parameters, assumptions, analytical choices, and projected principal financial impacts.

■ If a registrant uses an internal carbon price, information about the price and how it is set.

Disclosures Related to GHG Emissions

■ Direct GHG emissions (Scope 1) and indirect GHG emissions from purchased electricity and other forms of energy (Scope 2), separately disclosed.

■ Indirect emissions from upstream and downstream activities in a registrant’s value chain (Scope 3), if material, or if the registrant has set a GHG emissions target or goal that includes Scope 3 emissions, in absolute terms, not including offsets, and in terms of intensity.³

Disclosures Related to Registrant Disclosed Climate-Related Targets or Goals

■ The scope of activities and emissions included in the target, the defined time horizon by which the target is intended to be achieved, and any interim targets.

■ How the registrant intends to meet its climate-related targets or goals.

■ Relevant data to indicate whether the registrant is making progress toward meeting the target or goal and how such progress has been achieved, with updates each fiscal year.

■ If carbon offsets or renewable energy certificates (“RECs”) have been used as part of the registrant’s plan to achieve climate-related targets or goals, certain information about the carbon offsets or RECs, including the amount of carbon reduction represented by the offsets or the amount of generated renewable energy represented by the RECs.

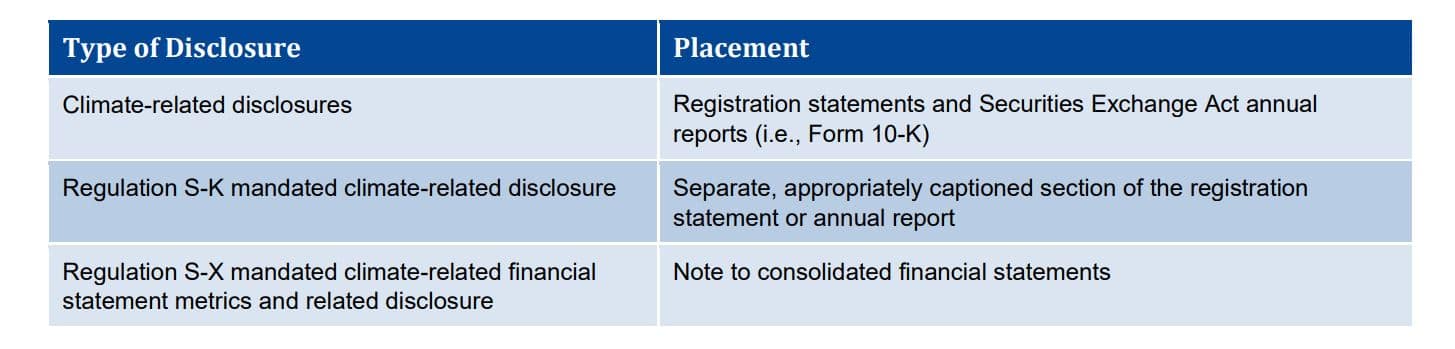

Presentation and Attestation of Proposed Disclosures

The proposed rules would require a registrant (including a foreign private issuer) to disclose climate related risk in accordance with the following table:

If an accelerated or large accelerated filer, registrant must obtain an attestation report from an independent attestation service provider covering, at a minimum, Scopes 1 and 2 emissions disclosures.

Phase-In Periods and Accommodations for the Proposed Disclosures

The proposed rules would include:

■ A phase-in period for all registrants, with the compliance date dependent on the registrant’s filer status, and an additional phase-in period for Scope 3 emissions disclosure.

■ A phase-in period for the assurance requirement and the level of assurance required for accelerated filers and large accelerated filers (see assurance table).

■ A safe harbor for liability for Scope 3 emissions disclosure.

■ An exemption from the Scope 3 emissions disclosure requirement for smaller reporting companies.

■ Forward-looking statement safe harbors pursuant to the Private Securities Litigation Reform Act, to the extent that proposed disclosures would include forward-looking statements.

Comment Period

Comments are due by the later of May 20, 2022 and the date 30 days after publication of the proposed regulations in the Federal Register.

¹ “We are not proposing a compensation-related disclosure requirement at this time, because we believe that our existing rules requiring a compensation discussion and analysis should already provide a framework for disclosure of any connection between executive remuneration and achieving progress in addressing climate-related risks.” [Proposal, p. 102.]

² In assessing whether a climate-relate risk is material, a registrant should consider the magnitude and probability of the specific risk over the short, medium, and long term. The SEC notes that, with regard to a transition risk yet to be realized, the magnitude of loss or liability may be high even if the probability of an adverse consequence is relatively low. Additionally, a registrant should assess whether a particular risk is information that a reasonable investor would consider important to an investment or voting decision.

³ When assessing the materiality of Scope 3 emissions, a registrant should consider whether Scope 3 emissions make up a relatively significant portion of its overall GHG emissions. However, even if Scope 3 emissions make up a relatively small portion of a registrant’s overall GHG emissions, they could be material if such emissions represent a significant risk, are the subject to significant regulatory focus, or “if there is a substantial likelihood that a reasonable [investor] would consider it important.”

* * * * *

The Client Update is prepared by Meridian Compensation Partners’ Technical Team led by Donald Kalfen. Questions regarding this Client Update or executive compensation technical issues may be directed to Donald Kalfen at 847-235-3605 or dkalfen@meridiancp.com.

This report is a publication of Meridian Compensation Partners, LLC, provides general information for reference purposes only, and should not be construed as legal or accounting advice or a legal or accounting opinion on any specific fact or circumstances. The information provided herein should be reviewed with appropriate advisors concerning your own situation and issues.

www.meridiancp.com