We expect further changes to be made in both the House and Senate tax proposals. Ultimately, any differences between the House and Senate proposals would need to be addressed during the reconciliation process.

This Update first summarizes the Senate tax proposal’s provisions relating to executive compensation and then compares the House and Senate tax proposals on corporate and individual income taxes.

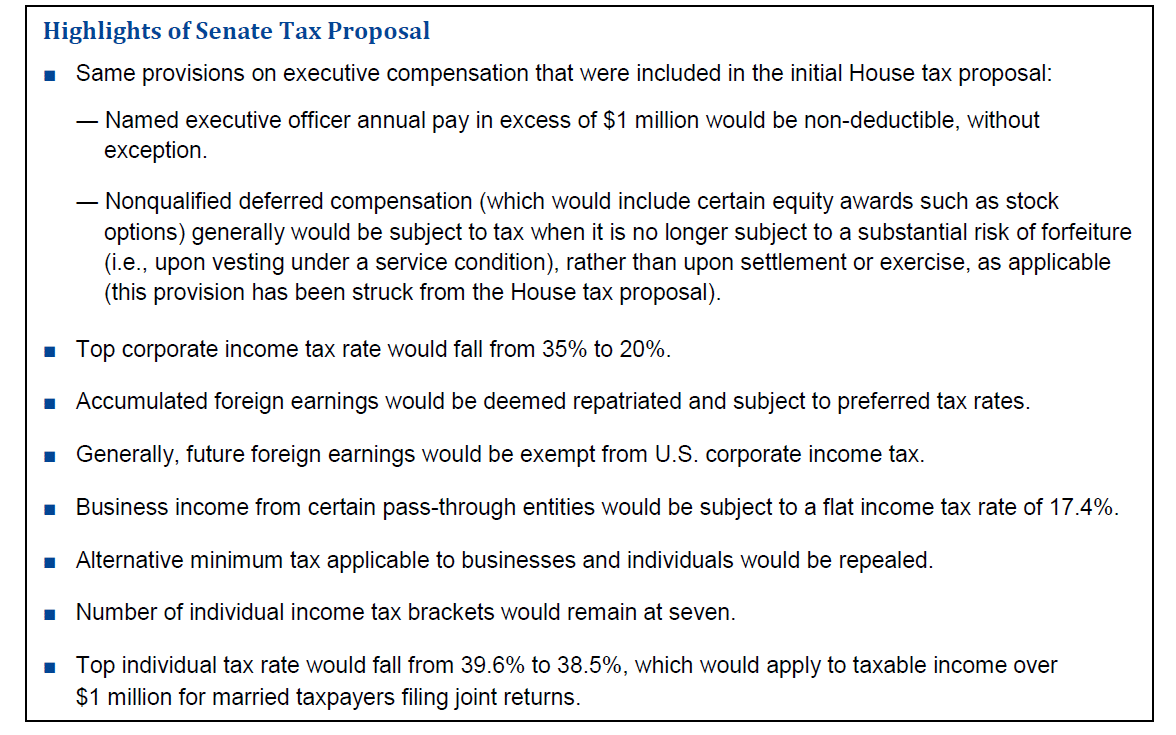

Provisions Relating to Executive Compensation

The Senate tax proposal includes the same provisions on executive compensation that were part of the initial House tax proposal: (i) change in tax treatment of nonqualified deferred compensation and (ii) modification to Code Section 162(m). These proposed changes to the Code are briefly discussed below. Please refer to our Client Update dated November 7, 2017 for a detailed summary and analysis of these proposed changes.

Proposed Change in Treatment of Nonqualified Deferred Compensation

Like the initial House tax proposal, the Senate tax proposal would require nonqualified deferred compensation (NQDC) to be subject to tax when such compensation is no longer subject to a substantial risk of forfeiture. Included in the definition of NQDC would be certain equity awards, such as restricted stock units, performance share units, performance units, nonqualified stock options and stock appreciation rights. The proposed changes in the tax treatment of NQDC would substantially affect the design and, in some cases, viability of certain compensation and retirement programs.

As we previously reported, late last week the proposed provisions related to NQDC were deleted from the House tax proposal. Therefore, it was somewhat of a surprise to see these provisions included in the Senate Republican’s tax proposal. However, given when the respective tax proposals were released, it would appear that the Senate Republicans simply replicated the provisions from the House tax proposal before they were deleted from the proposal. This suggests the absence of a champion for the NQDC provisions among Senate Republicans.

The open question is whether the Senate Republicans will follow the actions of their House colleagues and remove the NQDC provisions from the Senate tax proposal. This question may be answered as soon as this week. If the status quo is left unchanged, then the fate of the NQDC provisions would be decided during the reconciliation process.

Proposed Modification to Code Section 162(m)

Like the House tax proposal, the Senate tax proposal would make the following modifications to Code Section 162(m):

■ Eliminate the exception to the $1 million deduction cap for performance-based compensation (e.g., compensation linked to the achievement of shareholder-approved performance metrics, grant of compensation committee approved nonqualified stock options).

■ Revise the definition of a covered employee to include the principal financial officer (in addition to the principal executive officer and three highest-paid proxy-disclosed officers other than the principal executive officer and principal financial officer).

■ Once an individual qualifies as a covered employee, the $1 million deduction cap would apply to that person so long as the corporation pays remuneration to such person (or to any of that person’s beneficiaries).

The proposed modification to Code Section 162(m) would be effective for taxable years beginning after December 31, 2017.

The proposed modification does not explicitly grandfather compensation paid to a covered employee after the effective date but that was earned over a multi-year performance or service period that began before the effective date. Without statutory or regulatory relief, arguably incentive compensation earned under currently outstanding performance cycles (including performance cycles ending on December 31, 2017) but paid after December 31, 2017 could be subject to the proposed modification to Code Section 162(m).

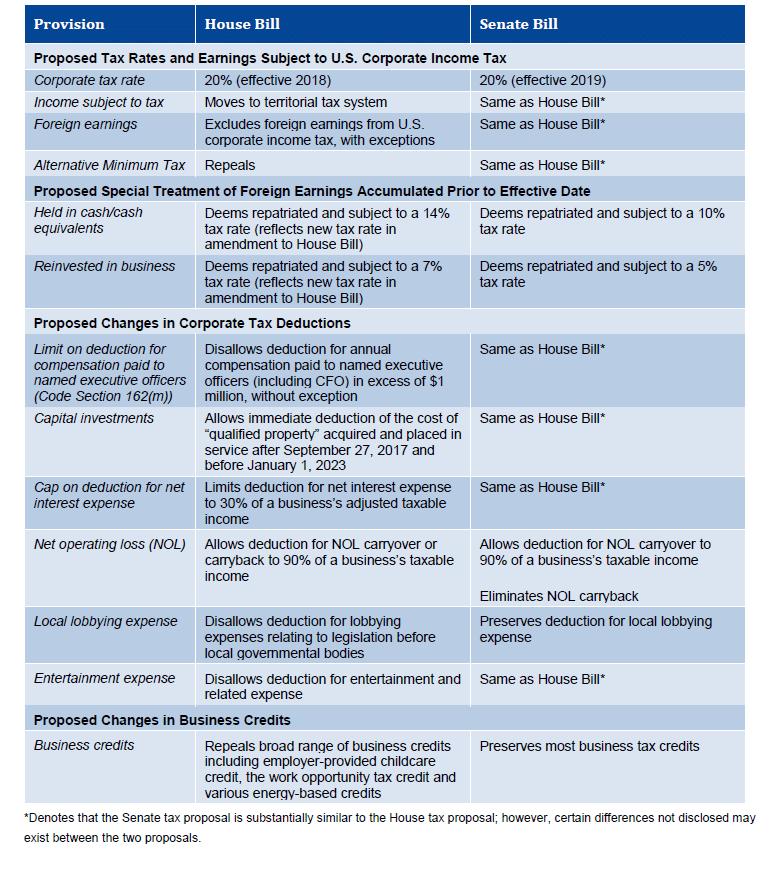

Comparison of House and Senate Tax Proposals on Corporate Income Tax

The chart below compares key elements of the House and Senate tax proposals on corporate income tax.

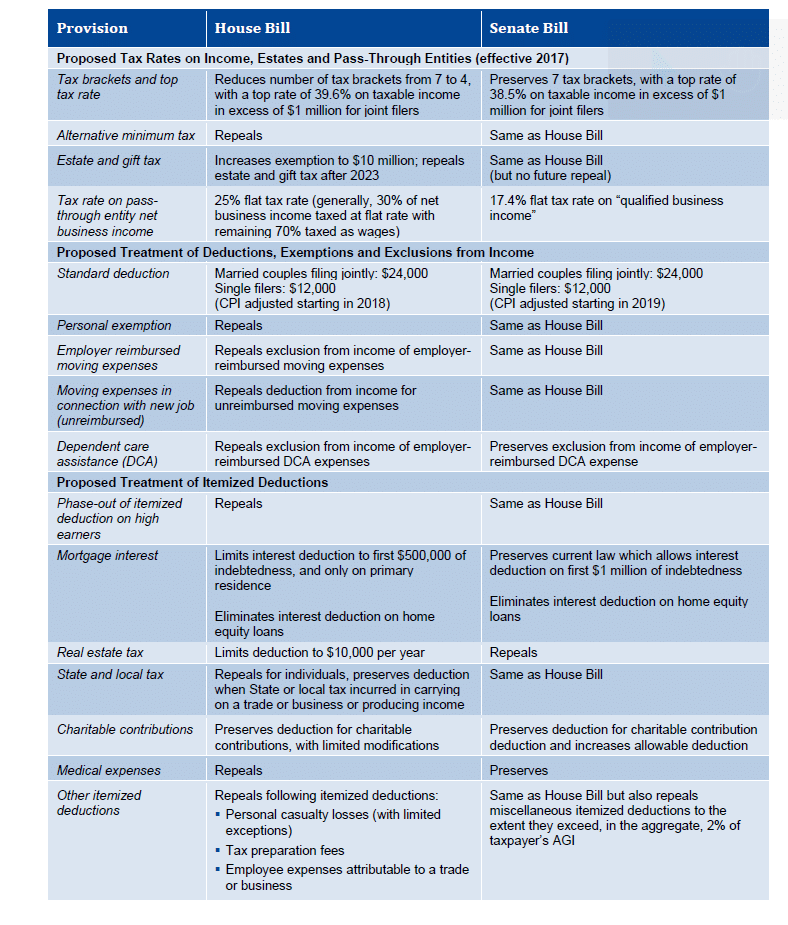

Comparison of House and Senate Tax Proposals on Individual Income Tax

The chart below compares key elements of the House and Senate tax proposals on individual income tax.

* * * * *

The Client Update is prepared by Meridian Compensation Partners’ Technical Team led by Donald Kalfen. Questions regarding this Client Update or executive compensation technical issues may be directed to Donald Kalfen at 847-235-3605 or dkalfen@meridiancp.com.

This report is a publication of Meridian Compensation Partners, LLC, provides general information for reference purposes only, and should not be construed as legal or accounting advice or a legal or accounting opinion on any specific fact or circumstances. The information provided herein should be reviewed with appropriate advisors concerning your own situation and issues.

www.meridiancp.com