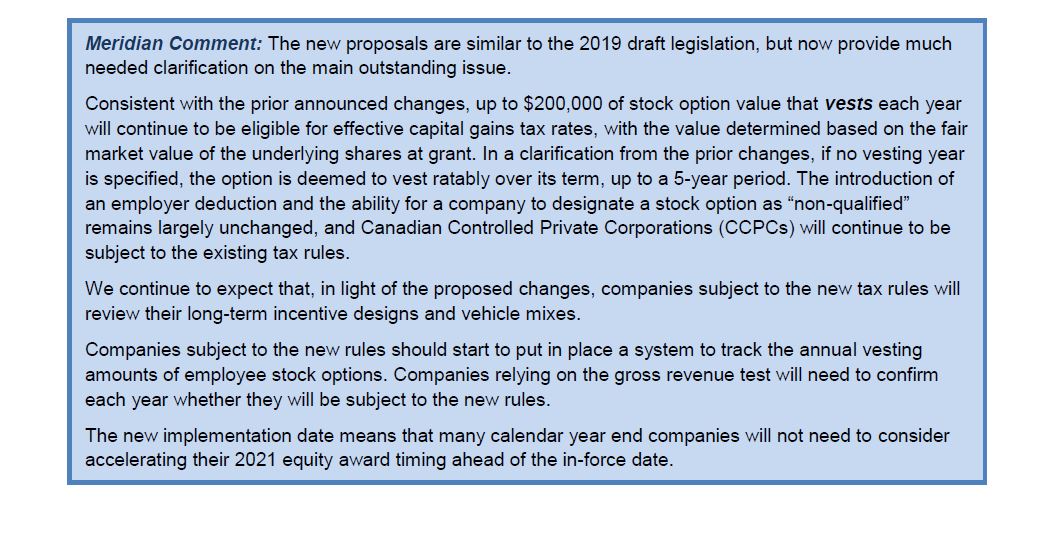

As part of the federal government’s Fall Economic Statement, the Department of Finance announced a new implementation date for the planned change to the taxation of stock option gains, and clarified who will continue to be eligible for effective capital gains tax rates on the exercise of options.

As discussed in earlier Meridian client updates (available June 2019 here, and March 2019 here), the federal government announced in 2019 a planned change to the tax treatment of stock option gains. The initial proposal eliminated the effective capital gains tax treatment on stock option gains, for most option awards at most companies, resulting in those option gains being subject to ordinary income tax rates. The main outstanding issue was how the government would define “start-up, emerging, and scale-up” companies, which would still be eligible for the existing effective capital gains treatment. In late 2019, the Department of Finance delayed the implementation date for the new stock option tax rules.

The federal government has now proposed the following:

- The new tax rules will take effect for grants made on or after July 1, 2021. Grants made before that time will be subject to the existing rules and continue to be eligible for effective capital gains treatment.

- The existing effective capital gains treatment will also remain in place for stock options granted at companies with annual gross revenues of $500 million or less at the time of grant (i.e., companies that are “start-ups, emerging or scale-up companies”). The revenue limit is applied on an annual basis, and for an employer that is a member of a corporate group, at the highest level of consolidation, and is based on the last annual financial statements presented to shareholder.

* * * * *

The Client Update is prepared by Meridian Compensation Partners. Questions regarding this Client Update or executive compensation technical issues may be directed to:

Christina Medland at (416) 646-0195, or cmedland@meridiancp.com

Andrew McElheran at (416) 646-5307, or amcelheran@meridiancp.com

Andrew Stancel at (647) 478-3052, or astancel@meridiancp.com

Andrew Conradi at (416) 646-5308, or aconradi@meridiancp.com

Matt Seto at (416) 646-5310, or mseto@meridiancp.com

This report is a publication of Meridian Compensation Partners Inc. It provides general information for reference purposes only and should not be construed as legal or accounting advice or a legal or accounting opinion on any specific fact or circumstances. The information provided herein should be reviewed with appropriate advisors concerning your own situation and issues.

www.meridiancp.com