The election of Donald J. Trump as the next President of the United States will likely have far reaching effects on the statutory and regulatory regimes covering executive compensation and related corporate governance matters.

What exactly the effect will be remains to be seen. However, based on published materials on President-elect Trump’s website, public statements by Mr. Trump and his staff and related media reports, we will attempt to prognosticate on future developments.

Changes at the Securities and Exchange Commission (SEC)

One thing is certain, Republican Commissioners will control the SEC and its agenda starting in 2017. Recently, SEC Chair Mary Jo White announced her resignation from the SEC effective as of the last day of President Obama’s term. This clears the way for President-elect Trump to appoint the next Chair of the SEC.

In addition to Chair White’s departure in 2017, current Commissioner Kara Stein will be leaving the SEC when her term expires in August 2017, unless she is reappointed by President-elect Trump. That will leave Michael Piwowar as the sole holdover Commissioner. Customarily, three of the five SEC Commissioners are affiliated with the political party that holds the White House. This means that Mr. Trump may appoint two Commissioners (i.e., the Chair and a member) who are affiliated with the Republican party (current Commissioner Piwowar is affiliated with the Republican party). The two other vacant seats would be filled by Commissioners who are affiliated with the Democratic party.

The process of selecting and confirming new Commissioners could drag into the Summer of 2017. Until such time, the SEC will be at a virtual standstill in terms of proposing new rules and adopting final rules. This delay will have significant implications with regard to the open Dodd-Frank executive pay mandates (see below discussion).

The Fate of Dodd-Frank Mandates on Executive Pay Hang in the Balance

Many in the business community are hopeful that the CEO pay ratio rule will be abandoned under a Trump administration’s dismantling of Dodd-Frank. In fact, the election puts in play all of the Dodd-Frank mandates on executive pay. These include Say on Pay, compensation committee independence standards, various pay disclosures and mandatory recoupment policy. Mr. Trump’s proposed reformation of Dodd-Frank could cause each of the mandates to be put out of existence.

De-regulation versus populism, which will win out? Mr. Trump’s apparent populist views on CEO pay may override his de-regulation instincts when it comes to the executive pay mandates, particularly the CEO pay ratio rule. However, the issue of CEO pay was not front and center during the campaign. Therefore, Mr. Trump’s views on CEO pay from a regulatory perspective are not known.

The view from the Republican establishment. Advising Mr. Trump on Dodd-Frank is Jeb Hensarling (R-Texas), the Chair of the House Financial Services Committee. Rep. Hensarling, a staunch critic of Dodd-Frank, may serve as a counterweight to populists views on the executive pay mandates. Mr. Hensarling has already addressed these mandates through his Dodd-Frank replacement bill, the Financial Choice Act of 2016 (FCA), which was approved by the House Financial Services Committee on September 13, 2016. The FCA would leave unchanged the compensation committee independence standards and the pay-for-performance disclosure, modify Say on Pay and mandatory recoupment requirements and repeal the CEO pay ratio, bank pay rules, disclosure on hedging, proxy access and disclosure on CEO and Board chair structure. Of course, a complete repeal of Dodd-Frank (without replacement) would result in the repeal of each of the executive pay mandates.

Regardless of whether Dodd-Frank is modified or replaced, the FCA shows at least rank and file Republicans (if not Mr. Trump) prefer to eliminate some but not all of Dodd-Frank’s executive pay mandates.

Our prognostication on the fate of the Dodd-Frank executive pay mandates. Based on this somewhat muddled picture, here is our best guess on the future of the executive pay mandates under Dodd-Frank:

| Dodd-Frank Provision | Probability of Repeal |

|---|---|

| Proxy Access | High |

| Disclosure on CEO/Board Chair Structure | High |

| Mandatory Recoupment | Medium |

| CEO Pay Ratio | Medium |

| CEO Pay-for-Performance Disclosure | Medium |

| Hedging Disclosure | Medium |

| Bank Pay Regulations | Low to Medium |

| Compensation Committee Standards | Low |

| Say on Pay | Low |

The SEC Assumes a Bystander Role. Any hope is misplaced that the post-inaugural SEC will stop the CEO pay ratio or provide other relief from one or more other Dodd-Frank executive pay mandates. The SEC, as reconstituted following Mr. Trump’s assumption of office, will be reduced to a wait and see role pending the disposition of Dodd-Frank. Until then, the SEC clearly would not want to jump the gun by issuing final rules on open Dodd-Frank mandates that might be repealed or modified. The SEC is under no legal obligation to issue those final rules by any particular date. Additionally, unless otherwise instructed by the Trump White House, it is highly unlikely that the SEC, on its own initiative, would repeal its rules on the CEO pay ratio or any other final rule on the executive pay mandates. However, depending on the status of the Dodd-Frank overhaul, it is conceivable the SEC could be instructed to delay the effective date of the CEO pay ratio to 2018 or beyond.

Public companies must assume CEO Pay Ratio will go into effect. The CEO pay ratio rule is set to take effect in 2017, with the first disclosure reported in 2018 proxies. Its ultimate fate remains uncertain. Until the position of the future Trump administration crystallizes on this issue, we recommend that companies proceed under the assumption that the CEO pay ratio will go into effect in 2017, with initial disclosures in 2018.

Federal Tax Rates Are Headed Lower

Whether there is full blown Federal tax reform is unclear; however, it is a near certainty that marginal tax rates for individuals and tax rates for corporations will be declining under the Trump Administration.

Tax Rate Proposals

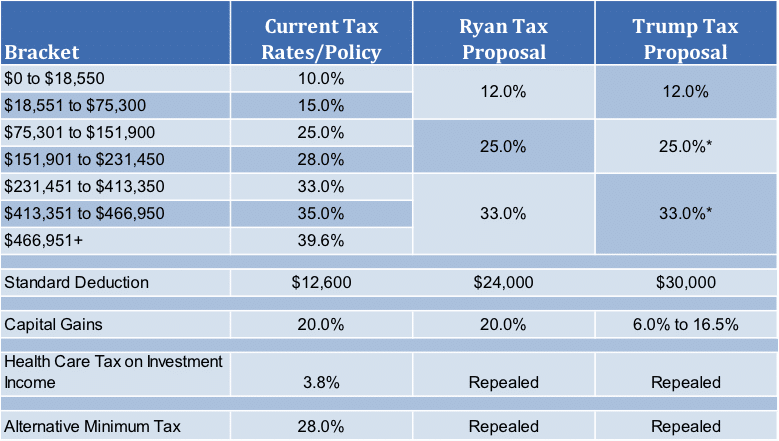

Both President-elect Trump and Speaker Paul Ryan (R – Wisconsin) have offered similar blueprints for reducing marginal rates and altering other tax provisions on individual taxpayers, as shown in the below chart (for married couples filing jointly).

*Under the Trump tax proposal, the second and third income brackets slightly differ from those shown in the above chart.

In addition, President-elect Trump’s and Speaker Ryan’s proposed tax plans would reduce the corporate tax rate from a flat 35% to a flat 15% and a flat 20%, respectively. Both proposals would repeal the corporate and alternative minimum tax.

Simplification of Tax Code

Both the Trump and Ryan proposals call for simplification of the tax code. However, the Trump plan is relatively light on specifics (beyond those described above). The Ryan plan includes a number of features that will simplify the tax code for individual tax payers (e.g., limit on deductions, consolidation of standard deductions and personal exemptions). In addition, the Ryan plan includes a number of business-favorable features, such as immediate deduction for capital expenditures and indefinite carry-forward of net operating losses. However, the Ryan plan does not provide significant detail on simplification of the tax code for businesses.

The Trump and Ryan proposals are good starting points in simplifying the tax code. Whether the plans merge and evolve into a true overhaul and simplification of the tax code, particularly for corporate taxpayers, is unclear. As of now, any celebration of the potential demise of the three key areas of the tax code (i.e., 162(m), 280G and 409A) that regulate executive and employee compensation would be premature.

Nothing Will Come Easy

President-elect Trump’s ambitious agenda will surely meet stiff resistance from the Democrats in Congress. Notably, the Republicans do not have a filibuster proof majority in the Senate. This means that the Democrats could effectively block many of Mr. Trump’s most significant legislative initiatives in the Senate. Mr. Trump may have to compromise on a number of legislative positions to gain sufficient support from Senate Democrats to avoid the threat of a filibuster (or stop an ongoing filibuster). However, the Republicans do have available certain parliamentary procedures that could potentially work through a filibuster. All of which means the 2017 legislative session is shaping up to be very interesting.

* * * * *

The Client Update is prepared by Meridian Compensation Partners’ Technical Team led by Donald Kalfen. Questions regarding this Client Update or executive compensation technical issues may be directed to Donald Kalfen at 847-235-3605 or dkalfen@meridiancp.com.

This report is a publication of Meridian Compensation Partners, LLC, provides general information for reference purposes only, and should not be construed as legal or accounting advice or a legal or accounting opinion on any specific fact or circumstances. The information provided herein should be reviewed with appropriate advisers concerning your own situation and issues.

OUR HUMBLE PREDICTIONS