Find this article and more in the most recent issue of Equilar C-Suite magazine. Find past issues of C-Suite at Equilar.com.

Boards walk a fine line to align director pay with shareholder value

By Ryan Villard

Boards of directors bridge the gap between investors and their executive teams, providing guidance and holding management accountable for both successes and failures while working closely together to maximize company growth and shareholder value. In the wake of Dodd-Frank and increasing shareholder and proxy advisor scrutiny, this role has evolved, and risk management has taken a front seat. However, directors and their growing role continue to face the problematic task of setting not only management’s compensation, but also their own.

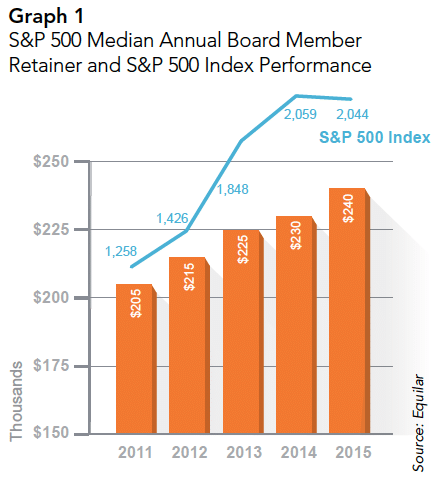

For these reasons, information and transparency have become paramount to best practices in director compensation. These practices enable boards to best situate their companies among their peers when making pay decisions, and then communicate those decisions to stakeholders. The Equilar report, Director Pay Trends 2016, featuring commentary from Meridian Compensation Partners, examined compensation trends for boards of directors at S&P 500 companies and found that the median director retainer including cash and equity increased 17.1% from $205,000 in 2011 to $240,000 in 2015 (Graph 1).

Pay and Progress

At first glance, this steady growth seems characteristic of annual pay raises matching market growth—however, while director pay grew steadily, markets performed exceptionally and expanded during this period. The S&P 500 index grew 62.5% from 2011 to 2015, shadowing director pay growth (Graph 1).

Not only did company performance exceed expectations, perspectives toward directors and their responsibilities expanded during this time. Boards both improved upon actively engaging shareholders and began facing new challenges such as managing cybersecurity risks and adapting to new regulations. While these new influential factors affected their workload, it didn’t necessarily affect their compensation.

“Compensation plans for corporate executives are specifically designed so that a significant portion of compensation actually earned is based on the financial and stock price performance of the company. Conversely, outside director pay plans are intentionally designed to be focused on annual periods and to not be performance-based,” explained Tom Ramagnano, partner with Meridian Compensation Partners. “Directors are often required to make important decisions related to the strategic direction of the company, decisions that could be viewed as ‘self-dealing’ if they result in an enhanced amount of compensation.”

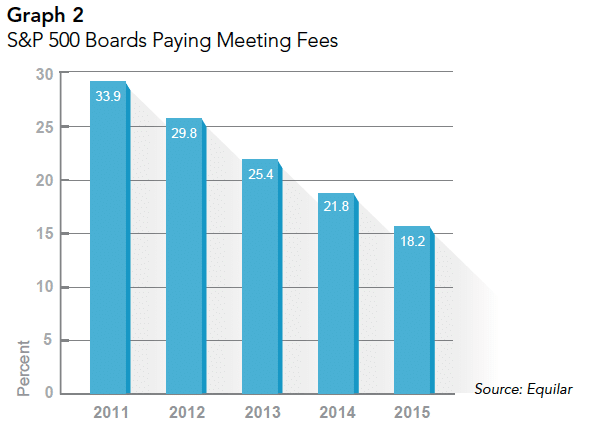

Similarly, attitudes around the director role shifted too, and their pay structures reflect this change. Payment of individual meeting fees declined significantly in the last five years—over one-third of S&P 500 boards paid meeting fees in 2011, vs. only 18.2% of companies in 2015. Part of their disappearance responds to directors’ growing responsibilities as they more frequently communicate through impromptu and brief meetings throughout the year, as opposed to once each quarter (Graph 2).

“The decreased prevalence of board and committee meeting fees is generally a reflection of how boards are now operating as a governing corporate body,” said Ramagnano. “In the past, decisions made by the board or committees tended to be ‘rubber stamped’ without much discussion or analysis. However, in the governance climate today, shareholders expect board members to be consistently engaged and focused on the company’s issues and to be well prepared and active participants at the meetings.”

While directors’ expanding role demonstrates their commitment to shareholders, these growing responsibilities affect their abilities to be on too many boards at once. While being on more than one board can be valuable in bringing unique experiences and perspectives, growing responsibilities increase the pressures of multi-boarding because directors may be stretching themselves too thinly by representing a handful of companies. As a result, this trend declined in 2016, as 51.0% of S&P 500 board seats were occupied by directors who served on more than one board, compared to 53.2% in 2015, according to Equilar data.

Board Structure and Pay Vehicles

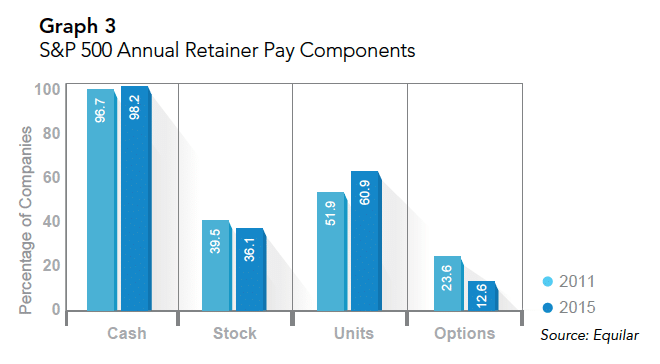

Director pay typically takes the form of cash, stock, options or restricted stock units (RSUs). Historically, cash has been a nearly universal pay vehicle, appearing in 98.2% of director pay packages in 2015 and remaining largely present across the entire study. Since 2011, the number of companies offering restricted stock or options as compensation fell. The former decreased minimally, dipping from 39.5% in 2011 to 36.1% in 2015, and the latter—mirroring its decline in executive compensation—nearly halved, tumbling from 23.6% in 2011 to 12.6% in 2015. On the other hand, prevalence of restricted stock units grew nine percentage points from 51.9% in 2011 to 60.9% in 2015 (Graph 3).

RSUs are simpler full-value stock vehicles that allow for more flexibility and tax deferral possibilities compared to options, while also better aligning directors with shareholders because they are plainly shares, rather than the opportunity to purchase shares.

The recent shift toward RSUs reflects board restructuring since the financial crisis as a majority of boards began shifting from classified to declassified. Equilar found that the prevalence of classified boards in the S&P 500 decreased from 27.9% in 2012 to 10.4% in 2016. Declassified boards require directors to be reelected annually whereas classified boards have varying term lengths—consequently, these positions are becoming single-year commitments, and their pay structures are changing to reflect this shift by relying less on option awards.

“The shift that we’re seeing away from options can be connected to board governance shifting away from classified boards,” said Ramagnano during Equilar’s Director Pay: Boardroom Changes Shift Compensation Philosophy webinar. “[Director] pay is taking on a one-year perspective and, since options are appreciation-only vehicles, they are a much longer-term vehicle. They fit well when we had classified boards and directors were elected with three-year terms, and there was time for those options to vest based on a long-term focus.”

Litigation on Director Pay

In the last few years, shareholders have filed lawsuits against boards, citing that excessive pay contributes to general corporate waste and breaches their fiduciary duties to shareholders. Often these stakeholders are successful, and boards are looking to protect themselves from this litigation by introducing meaningful director pay caps that limit cash and equity compensation.

“The limit should be some multiple of director compensation at the company, with boards looking at what they are paying now, and what their peers are paying to determine if their pay is reasonable,” said Megan Arthur Schilling, an associate at Cooley, during the Equilar webinar. “We typically see in our analysis a limit of two to five times, but I expect that will come down to around two to three as these lawsuits make clear that limits beyond three times might not be considered reasonable.”

According to an Equilar study, 28 S&P 100 companies have disclosed a director pay cap, and about half of these fell within a multiple of two to three times their median compensation. These caps spanned from $400,000 to $2.0 million.

Boards have responded to growing scrutiny around director pay by increasing transparency and shareholder engagement, and this will continue to be a hot-button issue in 2017. Changes to director compensation plans are a priority among governance practitioners looking toward the creation of appropriate director pay caps. If the heat continues to rise on this topic, it could perhaps catalyze new regulations such as say on director pay.

Contributors

- Tom Ramagnano, Partner, Meridian Compensation Partners

- Megan Arthur Schilling, Associate, Cooley