Study Group Characteristics and Report Scope

Study Group Characteristics

Each of the 160 companies in the Study Group was a component company of the Standard & Poor’s 500® Index1 (“S&P 500®”) as of December 31, 2016. In addition, the Study Group includes companies from each of the major industrial sectors covered by the S&P 500®. Overall, the Study Group reflects a reasonable cross-section of industries that comprise the Index. We believe the results of the Study are representative of CIC severance practices across the entire S&P 500®.

The composition of the 2017 Study Group is similar to the 2014 Study Group. Of the 160 companies included in the 2014 Study Group, 135 of these companies are part of the 2017 Study Group. The remaining 25 companies were not included in our 2017 Study Group because they were not component companies of the S&P 500® on December 31, 2016. To enhance the validity of the Study’s trends comparisons, each of these 25 companies was replaced by a similar S&P 500® company in terms of industry, revenue and market capitalization.

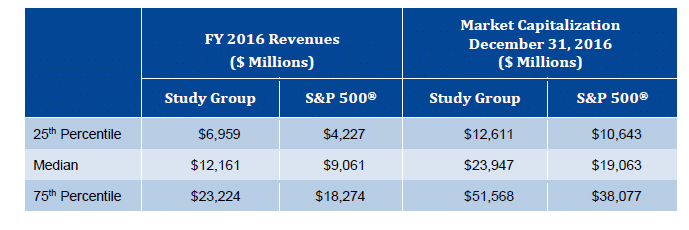

Displayed below are revenue and market capitalization statistics for the 2017 Study Group.

Report Scope

This Study reports on the prevalence of executive CIC arrangements that cover named executive officers (“NEOs”). In addition, the Study reports on the prevalence of the following components of executive severance and other benefits payable to NEOs in connection with a CIC:

■ Cash Severance Benefits

■ Responses to Potential Imposition of Golden Parachute Excise Tax

■ Vesting of Equity Awards in Connection with a CIC

Importantly, the Study does not report on benefits that may be payable to an NEO upon a termination of employment not in connection with a CIC or capture potential enhancements in, or modifications to, severance benefits that may be negotiated upon an actual termination in connection with a CIC.

Development of Study Group Statistics

We derived data and information for this Study primarily from the definitive proxy statements filed by each company in the Study Group with the Securities and Exchange Commission (“SEC”). We also derived data and information from publicly disclosed employment agreements, CIC agreements/plans and equity incentive plans and award agreements covering NEOs of the Study Group.

For the most recent year of data, we examined proxy statements filed primarily in calendar year 2017 that cover CIC arrangements in effect during fiscal year 2016. Data referenced from our 2014 Study follows a similar pattern. Throughout this Study, we reference data according to the fiscal year covered by the proxy statement, not according to the year in which the proxy statement was filed with the SEC.

Where meaningful, the Study shows separate prevalence statistics for each NEO (i.e., chief executive officer (“CEO”), chief financial officer (“CFO”) and the three highest paid NEOs other than the CEO and CFO). The Study refers to the three highest paid named executive officers other than the CEO and CFO as NEO #3, NEO #4 and NEO #5 in descending order of reported compensation.

Overview of Change-in-Control (CIC) Arrangements

CIC arrangements remain a common practice among large public companies in North America. Typically, these arrangements cover a company’s top executive officers and provide, at a minimum, cash severance benefits upon a triggering event. Other frequently provided CIC-related benefits include continuation of health care benefits, payment of current year bonus, enhancement to retirement benefits and outplacement services. The payment of these benefits and cash severance are nearly universally triggered upon an NEO’s qualifying termination of employment (i.e., termination without “cause” or termination for “good reason”) that occurs within a specified “protection period” (typically 24 months) following a CIC (i.e., “double-trigger vesting”).

Generally, the most valuable and perhaps the most controversial CIC benefit is the treatment of non-vested long-term incentive awards. Historically, the majority practice was to vest and settle non-vested long-term incentive awards solely upon the occurrence of a CIC (i.e., single-trigger vesting). Due to mounting pressure from proxy advisors (particularly Institutional Shareholder Services) and some institutional shareholders, the majority of large public companies have moved from single-trigger vesting to double-trigger vesting (or a variant of double-trigger vesting) of long-term incentive awards.

Finally, CIC arrangements at one time commonly provided for excise tax gross-up payments in the event that an executive officer’s CIC benefits were subject to the 20% excise tax applicable to “excess parachute payments.” That is no longer the case as excise tax gross-up provisions have declined sharply in prevalence and become a relatively small minority practice.

Purpose for CIC Arrangements

Generally, CIC arrangements cover executive officers for the following reasons:

■ Keep the Executive Neutral to Job Loss. The primary purpose for CIC arrangements is to keep senior executives focused on pursuing all corporate transaction opportunities that are in the best interests of shareholders, regardless of whether those transactions may result in their own job loss.

■ Retain Key Talent. Corporate transaction activity may create uncertainty for critical executive talent. This uncertainty may create significant retention risk for a company. An executive with sufficient severance protection may be less likely to leave voluntarily to seek other employment in the face of transaction-related uncertainty.

■ Maintain Competitive CIC Benefits. A majority of large public U.S. companies provide their senior executive officers with some level of CIC protection. Thus, companies provide CIC protection to attract and retain the top talent, especially in industry sectors undergoing substantial change or consolidation.

Forms of CIC Arrangements

CIC arrangements generally take the form of either a single CIC plan or policy that provides CIC protection to a group of executives, or individual employment contracts or severance agreements. The use of a single CIC plan or policy is increasing in prevalence for a number of reasons. Typically, companies find a single CIC plan easier to administer, revise and communicate than individual agreements. Further, a single plan approach ensures uniformity of terms and provisions for all covered executives, which is not always the case with individual agreements (often unintentionally).

In addition to a single CIC plan or individual CIC agreements, other arrangements may also provide CIC benefits to executives. For example, equity incentive plans or applicable award agreements often provide for the treatment of outstanding equity awards in connection with a CIC (e.g., acceleration of vesting in connection with a CIC—either single- or double-trigger), and non-qualified deferred compensation plans may provide for the enhancement of plan benefits in connection with a CIC.

Executives Covered Under CIC Arrangements

Generally, a CIC arrangement covers senior executives directly involved in the identification, negotiation and execution of strategic corporate transactions and, to a lesser extent, other key executives that may be at particular risk of job loss in the event of a CIC. Based on our experience, we have seen a downward trend in the number of executives covered by a company’s CIC arrangements. Often, CIC arrangements solely cover a company’s CEO and the CEO’s direct reports. However, equity plans or award agreements that provide CIC benefits (e.g., vesting of long-term incentive awards upon a CIC) typically cover all recipients of equity grants.

General Trends

CIC arrangements have been subject to intense scrutiny for over 20 years. The level of scrutiny intensified with the enhanced disclosure of CIC arrangements brought about by multiple amendments to the proxy disclosure rules. These rules require extensive and detailed disclosure of payments and benefits provided to NEOs in connection with a CIC (as well as certain employment termination scenarios). Since the adoption of these new disclosure rules, activist shareholders, proxy advisory firms, institutional investors, corporate governance experts and media pundits have pressed companies to change key elements of their CIC arrangements. In 2011, these constituents gained additional influence through the start of shareholder advisory votes on both executive pay packages and CIC arrangements in the context of mergers and other corporate transactions.

This external pressure has caused many large public companies since our 2011 Study to:

■ Reduce cash severance multiples,

■ Eliminate single-trigger vesting of equity awards in favor of double-trigger vesting, and

■ Eliminate excise tax gross-ups and modified tax gross-ups.

Comparison to General Severance Benefits

To have a complete understanding of CIC arrangements, it is important to understand the similarities and differences between such arrangements and general severance arrangements. General severance and CIC arrangements are broadly similar, as both provide executive officers severance benefits upon the occurrence of a payment trigger. In addition, both arrangements may include restrictive covenants and condition the payment of benefits upon the execution of a release and waiver of claims. Typically, these arrangements coordinate the payment of benefits so that an executive may not draw benefits under both arrangements.

Despite the foregoing similarities, CIC arrangements and general severance arrangements differ in many material respects. For example, the benefits provided under CIC arrangements are typically greater than the benefits provided under a general severance arrangement. In addition, the payment of general severance benefits is commonly triggered solely upon an executive’s qualifying termination of employment (e.g., involuntary termination without cause) while payment of most CIC benefits requires the occurrence of a CIC and an executive’s qualifying termination of employment following the CIC.

Another important distinction between CIC arrangements and general severance arrangements relates to the protection that the former provides to an executive officer. At a minimum, CIC arrangements protect an executive officer’s severance benefits from diminution during a specified period following a CIC. In contrast, an executive officer’s general severance benefits may be at risk of reduction or termination following a CIC.

Key Findings

Summarized below are the Study’s key findings.

CIC-Related Cash Severance Benefits

The prevalence of Study Group companies that provide CIC-related cash severance benefits to NEOs has remained unchanged since 2013, with approximately three-quarters of the Study Group companies providing such benefits to their NEOs.

CIC Cash Severance Formula

Unchanged since 2013, every Study Group company that provides CIC-related cash severance benefits to NEOs determines cash severance based on a multiple of “compensation.” Nearly all companies define compensation as the sum of an NEO’s base salary and annual bonus, with annual bonus typically linked to target bonus.

Cash Severance Multiples

The prevalence of a 3× severance multiple has significantly declined since 2013 for NEOs. While a 3× severance multiple remains the majority (but declining) practice for CEOs, a 2× severance multiple is now the majority practice for CFOs and other NEOs.

Response to Imposition of Golden Parachute Excise Tax

As expected, since 2013 the prevalence of full or modified excise tax gross-up provisions in CIC arrangements declined significantly from 35% of companies in 2013 to 15% of companies in 2016. In contrast, “best net” provisions have surged in popularity increasing from 47% of companies in 2013 to 76% of companies in 2016.

Vesting of Equity Awards in Connection with a CIC

Approximately 98% of Study Group companies accelerate the vesting of at least one type of equity award in connection with a CIC, up from 95% of Study Group companies in 2013.

The prevalence of single-trigger vesting (i.e., vesting solely upon a CIC) of equity awards in connection with a CIC continued its sharp decline across all award types, with double-trigger vesting (i.e., vesting upon a qualifying termination of employment following a CIC) now the majority practice.

■ For all award types, the prevalence of single-trigger vesting has dropped from approximately 33% of companies in 2013 to less than 20% of companies in 2016.

■ In contrast, for time-based equity awards (stock options, restricted stock and RSUs), the prevalence of double-trigger vesting has increased from approximately 40% of companies in 2013 to over 60% of companies in 2016.

■ For performance shares, the prevalence of double-trigger vesting has increased from approximately 40% of companies in 2013 to over 52% of companies in 2016. Upon a triggering event, the majority practice is to vest performance shares at target (53% of companies) and pay the vested award in full rather than on a pro rata basis (77% of companies).

1 The S&P 500® Index is a registered trademark of Standard & Poor’s Financial Services, LLC, a part of McGraw-Hill Financial, Inc.

© 2017 Meridian Compensation Partners, LLC. The material in this publication may not be reproduced or distributed in whole or in part without the written consent of Meridian Compensation Partners, LLC.

Please contact Donald Kalfen at dkalfen@meridiancp.com or 847-235-3605 with questions or comments regarding this publication or to request a copy of the full report.